【Twyne】DeFi Lending Market Credit Line Delegation Layer / Lending unused borrowing capacity to others / Additional layers of DeFi will increase presence / @twynexyz

Expect further yields with DeFi Lending.

Good morning.

This is mitsui from web3 researcher.

Today, I researched about "Twyne".

☁️What is Twyne?

⚙️Detailed Structure

🚩Transition and Outlook

💬DeFi's additional layer of presence will increase

🧵TL;DR

Twyne is a "delegated layer of credit lines" built on top of DeFi lending markets such as Aave and Euler.

Lenders can lend their unused borrowing capacity to others, and borrowers can borrow more to increase capital efficiency.

For risk, a multi-layered safety design is introduced, including inherited clearing, loss allocation, and safety buffers.

Twyne, which aims to grow based on the cooperation with existing protocols, is an additional layered project that represents the second phase of DeFi.

☁️What is Twyne?

Twyne" is a universal "Delegation of Credit" in the DeFi Lending market on Ethereum.Twyne is a universal layer that enables "delegation of credit" in the DeFi lending market on Ethereum.Delegation of Credit".

Specifically, it operates as a non-custodial additional layer on top of existing protocols (such as Euler),marketplace where a lender's unused borrowing capacity (credit capacity) can be delegated to other users (borrowers) and utilized.This will allow the lender to

By doing this,lenders can earn additional yield from credit capacity that would otherwise lie unused.andborrowers can borrow more funds than on a regular platform or get a credit buffer to reduce liquidation riskThe borrower can borrow more funds or obtain a credit buffer to reduce liquidation risk than on a regular platform.

In the following section, we will explain the specifics of how this works, starting with the background (issues) of the existing lending market.

◼️The Existence of Idle Capital

In the DeFi Lending market, over 60% of the total borrowing capacity is left unutilized, contributing to low asset utilization and stagnant yields (APY).

This has resulted in the following situation

Those who want to borrow "want to borrow more but can't"

Those who are lending "are getting less yield on their assets on deposit"

The entire protocol is not capital efficient.

Behind this lies the structure of DeFi lending: existing lenders such as Aave and Euler limit the amount that can be borrowed against collateral (LTV), and many users do not actually borrow = "idle capital".

For example, even if 100 USDC is put up as collateral, only 70 USDC is actually borrowed, and the remaining 30 USDC worth of "borrowing capacity" exists unused by anyone.

However, this is a necessary feature to ensure safety in the highly volatile and anonymous crypto asset market.DeFi Lending cannot function safely if more funds are lent out and misused.

Therefore, "Twyne" is structured to make funds more efficient in a way that does not damage the safety of existing DeFi lending.

◼️ Delegation of borrowing capacity (credit lines)

Twyne creates new yield (Delegation APY) on idle capital by delegating unused lines of credit to borrowers, thereby increasing the overall yield for the lender.In addition to the base lending interest, the lender earns delegation fee income via Twyne, thus realizing a dual revenue stream of "protocol original interest + Twyne interest".

The borrower receives an additional credit supply via Twyne, thereby raising the borrower's loan-to-value (LTV) against the collateral above normal.

I will now explain in detail how it works, but the image is that of re-staking.Restaking receives additional yield by depositing proof of staking into the protocol, but Twyne also enables the delegation of credit lines by depositing proof of lending deposit tokens to achieve additional yield.

⚙️ detailed mechanism

Let's take a closer look at how it works.

We will look at it from two main aspects: the mechanics of how credit lines are delegated and safety considerations.

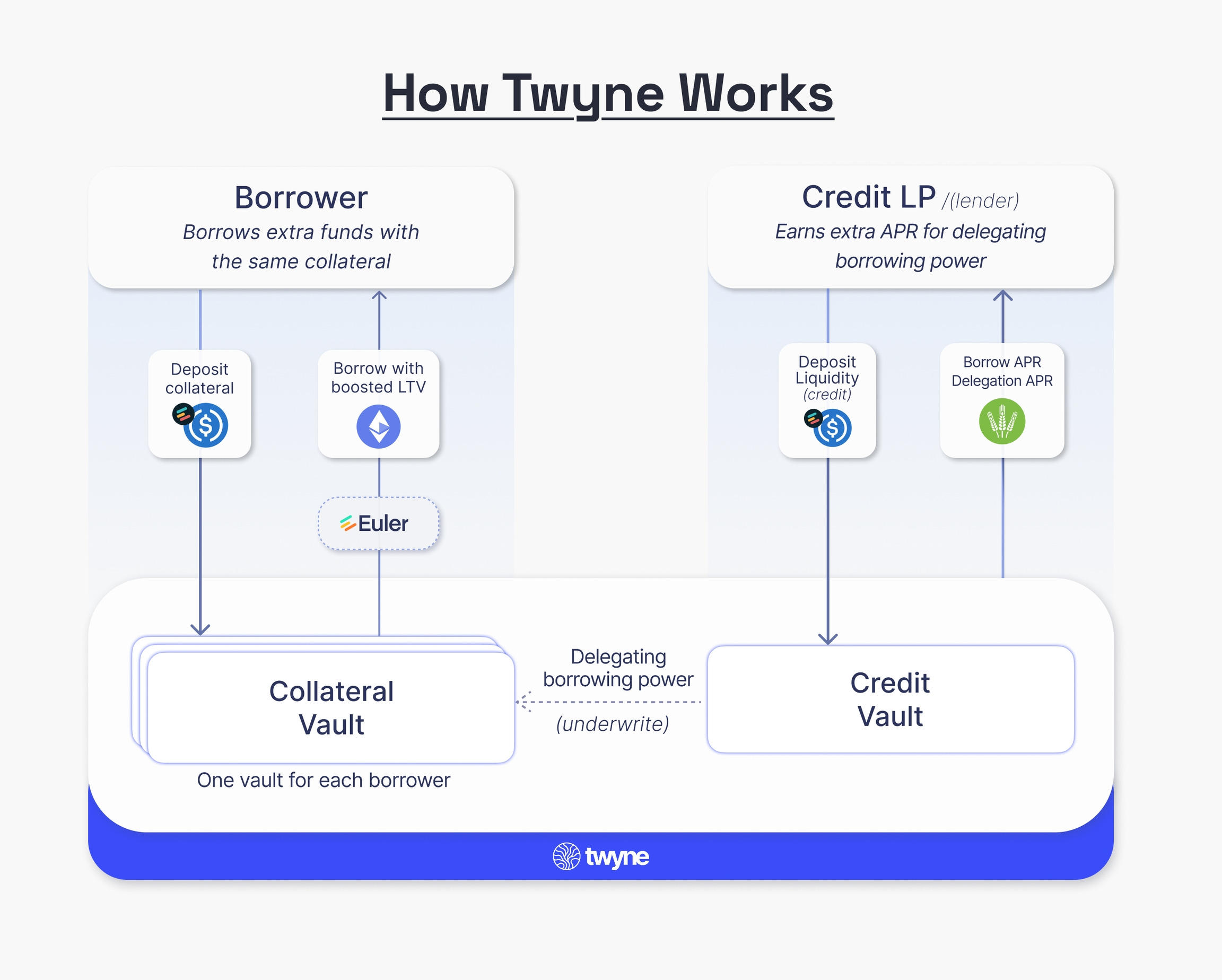

◼️ How to Delegate Credit Lines

The following is an explanation from the protocol flow.

Lender (Credit LP):

Supplies USDC and other funds to Aave and Euler (→ Get aUSDC, eUSDC)

Stake aUSDC in Twyne's Credit Vault

Credit Vault isonly the line of credit can be lent to the borrower (the asset itself is left on deposit)(the assets themselves are left on deposit).

Borrower:

Create your own Collateral Vault and deposit collateral (e.g. eWETH)

Make a "reservation of credit" from the corresponding Credit Vault (≈borrow a line of credit)

Borrow more than normal amounts from Aave and Euler (raising LTV)

Credit Vaults areA pool in which lenders stake receipts (aToken or eToken) and lend lines of credit,Collateral Vault is a pool in whichBorrowers deposit collateral and "reserve" credit from the Credit Vault to increase their borrowing limit.

The point here is that Twyne allows for more borrowing than foundational lending protocols such as Aave and Euler by "making it look like a user's collateral has been substantially increased.

By making good use of the "collateral judgment rules" of Aave and Euler smart contracts, LTVs are increased by temporarily adding the delegated credit as "sham collateral".This is called the "collateral judgment rule.This eliminates the need for any special notification or modification on the part of the lending protocol.

This mechanism does not allow Twyne to borrow and re-lend, but only exists as a delegation layer of credit.

◼️Safety

However, excessive borrowing naturally entails risk.So how does Twyne address that risk?

The first premise is that Twyne does not make any special modifications to Aave's side.Therefore, for regular lenders who simply deposit their assets in an underlying protocol such as Aave, the Twyne move will have no effect whatsoever.Only lenders who participate in Twyne assume the additional yield and risk.only those lenders who participate in Twyne assume the additional yield and risk.

With this design, Twyne has developed a unique liquidation method calledLiquidation by InheritanceThe "DeFi protocol" is built on the "DeFi protocol".This is very different from the forced-sale clearing done by the common DeFi protocol,This is a safety mechanism that aims to minimize the impact on the market.It is.

(1) Normal DeFi liquidation (e.g., Aave, Compound, etc.)

For example, suppose you had deposited 100 USDC as collateral and borrowed 95 USDC (LTV 95%).At this point, if the price of ETH or other securities falls and the LTV exceeds the liquidation line (e.g., 90%), the liquidator will force a sale of your collateral to collect the debt.

As a result, you lose your collateral, the market is pressured to sell, and the liquidator gets the difference (liquidation bonus).

(2) Twyne Liquidation: Liquidation by Inheritance

In contrast, Twyne does not "sell collateral" but rather takes the approach of "having the position (set of borrowing and collateral) passed on as is to other users.

For example, suppose that the borrower Alice's position has reached a risky level (LTV 95%) of 100 USDC for collateral / 95 USDC for borrowing.At this point, if Bob, the liquidator, decides that he would benefit from taking over the position, he will take over Alice's entire position.

Bob reconstitutes the position by adding 20 USDC of his own collateral, resulting in a safe position of "120 USDC of collateral / 95 USDC of debt (LTV approx. 79%)".

Thus,collateral is transferred to another user for the entire borrowing position without selling it in the market, thereby ensuring safety and reducing the impact on the market.This is a safe and effective way to minimize the impact on the market.

(3) External Liquidation (Fallback Liquidation)

However, if this succeeding liquidation does not occur and no one takes over the position, Twyne's borrower position will be subject to liquidation by the normal lending protocols (Aave or Euler).

In this case, the collateral is sold in the market,borrower's own collateral as well as some of the collateral delegated by the lender may be involved in the liquidation.This is positioned as the "worst-case" scenario in Twyne.This is positioned as the "worst case" in Twyne.

(4) Post-liquidation loss allocation logic (lender protection)

In the event of such an external liquidation, Twyne willreconfiguration logic to minimize losses.The system is equipped with a

Based on the assets recovered after liquidation, Twyne automatically reconfigures the borrower's Vault to "just under the maximum allowable LTV".In doing so, it firstThe borrower's own collateral is first reduced in priority, and the lender's collateral, which has been delegated to the borrower, is reallocated so that it is protected as much as possible.The borrower's own collateral is reduced in priority, and the lender's collateral that has been delegated is reallocated so that it is protected as much as possible.

This mechanism places borrowers in a "lock-in" situation where they cannot take out new loans and lenders aresignificantly reduce the risk of incurring unfair losses.(iv) Safety buffer (beta coefficient)

(5) Safety Buffer (Beta Factor)

In addition, Twyne introduces a "safety buffer (beta factor)" to address borrowers' positions before they are liquidated.This is accomplished by daring to set the maximum LTV set by Twyne lower than the liquidation threshold of the underlying protocol.

For example, if Aave and Euler require LTVs exceeding 90% to be liquidated, Twyne limits the maximum to 85-88%.Thereby,This allows room (grace) for Twyne's internal inheritance liquidation and rebalancing process before the liquidation line is reached.This safety buffer allows Twyne to manage risk more flexibly and smoothly.

The presence of such a safety buffer allows Twyne to manage risk more flexibly and smoothly, strengthening the mechanism to protect lenders from unexpected chain liquidation due to sudden price fluctuations, for example.

SUMMARY

While Twyne provides an innovative mechanism of credit delegation,safety for both lenders and borrowers, Twyne incorporates a four-step safety designThe following four-step safety design is incorporated to enhance the safety of both lenders and borrowers:

Liquidation by InheritanceLiquidation by Inheritance: position is taken over by another party without selling the collateral

External Liquidation (Fallback)Fallback: Recoverable through normal liquidation in the event of unsuccessful succession

Loss allocation and restructuring: Lenders' collateral is protected in priority after liquidation

Safety buffer (beta): Allows a margin of safety before clearing is triggered, allowing time for internal processing.

This allows Twyne to have a flexible and defensive risk management structure that was not previously available at DeFi, and a system that allows for the distribution of credit with peace of mind.

🚩Transition and Outlook

Twyne's development entity is a start-up company called Twyne Labs.Although the official date of establishment is not specified, the development team is composed of members who have been involved in consulting and research in the DeFi domain for many years.

Development of Twyne began around 2023, and it was selected as the "Best DeFi project on the Arbitrum chain" at the 2024 ETHDenver.(A test version has since been released at Base)

Currently still operating on an invite-only basis, Twyne has already attracted a high level of interest and support from professionals and the community.The company has received incubation support from Euler Labs (developer of the Euler lending protocol) since the development stage, and Euler Labs has expressed its support by stating that "Twyne is pushing the potential of credit delegation and leveraging idle capital to unlock the potential of the market.Euler Labs has expressed its support for Twyne.

In fact, in June 2025, Twyne raised a pre-seed funding round led by Euler Labs, totaling $450,000!

Lido, the largest staking protocol provider, has also taken notice of Twyne, and in April 2025, Twyne submitted a proposal to join the Lido Alliance (a strategic alliance framework for the Lido ecosystem).The proposal requested cooperation in protocol collaboration and promotion with Lido, saying that this would lead to greater use of stETH.As a reward, Twyne is offering 10% of the total supply of tokens issued in the future as a partnership incentive and locking in a 1-year cliff + 2-year vesting.

The roadmap for the future is a mainnet release by the end of 2025.After that, milestones such as achieving the TVL 5 million scale and completing the Morpho integration are set for the next 6 months or so.In the medium to long term, the company is also looking at supporting other chains and developing new product lines with more sophisticated credit intermediation.

💬DeFi's additional layer of presence will increase

Finally, a summary and discussion.

This was a very interesting project with a very interesting idea.Not surprisingly, when I look at the emerging DeFi these days, many of the players are solving their problems based on the assumption that existing DeFi players exist and function.

Perhaps the first phase of the DeFi war is already over to some extent, and the main functions such as DEX, Lending, etc. have been created to some extent.Of course, further development will continue, and I don't expect the market share to remain the same, but we are getting some of the right answers.

DeFi is moving on to the next second phase.While those existing DeFi's exist as a protocol, there is an additional layer that is emerging to solve the problems, like L2 in Ethereum.

Twyne is just such a project, which acts as an additional layer to the existing lending market.And we are pushing a strategy based on working with major DeFi such as Aave, Euler, Morph, and Lido from the beginning.

Personally, I also think this is an interesting aspect of blockchain: the composability world is constantly building up products, and late-start projects build their own positioning on the shoulders of the giants ahead of them.

Users then manage their own assets, determine their own risks, and use the products they like as they like.Since there is no enclosure such as user registration or data management, products are built up in a user-first manner.

The risk of spillover and settlement may increase as DeFi begins to work together, but looking at Twyne and other recent projects, there is a tendency for projects to not be evaluated unless they have some technical measures in place regarding settlement risk.At the very least, the design is such that it does not affect the existing market, and if anything happens, only the participants in the emerging protocols are at risk.That was rather the case with Restaking as well.

If the Twyne concept works, I'm looking forward to seeing the lending yield increase even more, and it will be a beneficial one for DeFi's stable investment portfolio.First of all, I would like to wait until the main net is released to the public.

This is my research on "Twyne"!

🔗Reference:HP / DOC / BLOG / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,'' we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter "web3 Research" delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.