【STBL】Next-generation stablecoin backed by real-world assets launched by Tether co-founder / Principal and interest claims separated as NFTs / @stbl_official

The Second Stablecoin Boom Has Arrived

Good morning.

I’m Mitsui, a web3 researcher.

Today I researched “STBL”.

What is STBL?

Characteristics of the Ecosystem

Transition and Outlook

The Second Stablecoin Boom Has Arrived

TL;DR

STBL is a “Stablecoin 2.0” protocol launched in 2025 by USDT co-founders, aiming to design a system that allows users to earn yields while using stablecoins.

A triple-token model where USST (stablecoin) and YLD (yield entitlement NFT) are simultaneously issued using RWA collateral, with STBL (governance token) handling voting, staking, and revenue redistribution (buybacks & burns, etc.).

Aiming to be the core of the “second wave of stablecoins” by maintaining the peg through overcollateralization + loss reserves + LAMP, ensuring regulatory compliance via KYC/whitelisting, and supporting the issuance of ESS by various companies as a MaaS solution.

What is STBL?

STBL is a next-generation stablecoin protocol dubbed “Stablecoin 2.0,” launched in 2025 by Reeve Collins, co-founder of Tether (USDT), and others.

Traditional stablecoins (e.g., USDT and USDC) allowed issuers to retain interest income generated from the backing assets, while users simply held tokens pegged to fiat currencies.

In contrast, the STBL protocol champions the principle of “Use Your Stablecoin, Keep Your Yield,” aiming to provide users with both the convenience of stablecoins and the interest income from their underlying assets.

Specifically, the aim is to evolve stablecoins from mere corporate products into public infrastructure by separating the principal value (stability) of assets from their yield, while further enhancing the transparency of reserve assets, yields, and governance.

Furthermore, this design philosophy also aims to achieve regulatory compliance by separating stablecoin and investment product elements, as required by certain U.S. legislation (the GENIUS Act).

◼️Mechanism

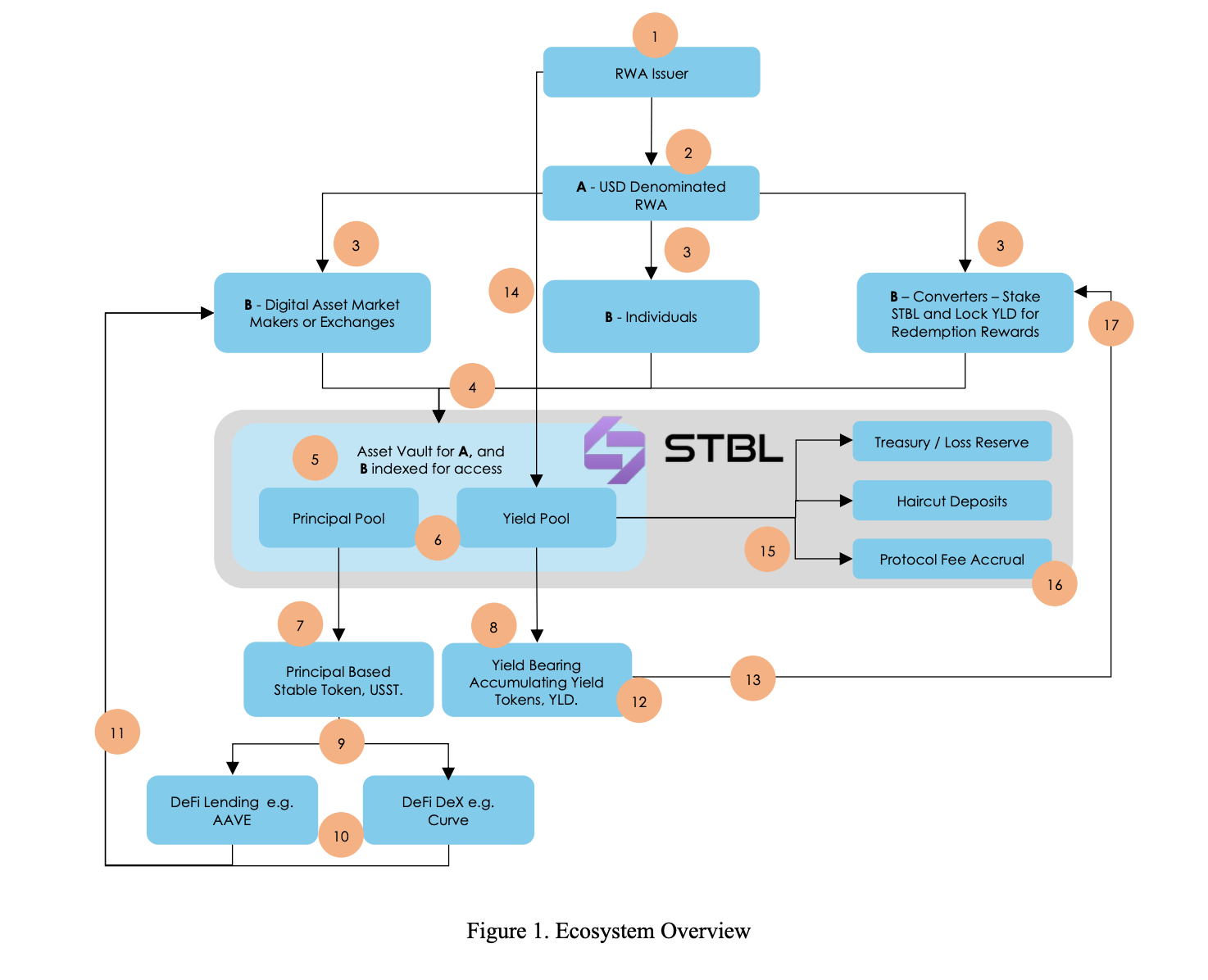

The STBL protocol is deployed on Ethereum and BNB, and its mechanism uses smart contracts to link three tokens.

These three tokens, while independent, complement each other to achieve stability, yield, and governance.

USST (Universal Stablecoin)

This is a stablecoin pegged to the US dollar. It is issued when users lock tokenized RWA (such as USDY or BUIDL) compatible with the protocol as collateral.

USST can be used for a wide range of purposes, including payments, trading pairs, DeFi operations, and value storage, as a stable medium of exchange.

We aim to become a universal payment layer that can be exchanged and interoperated 1:1 with the ecosystem-specific stablecoin (ESS) issued by partner companies described later.

YLD (Yield Rights NFT)

An NFT generated simultaneously with the issuance of USST, representing the right to claim interest and revenue generated from the corresponding collateral assets.

For example, if a user issues USST using a 5% annual interest government bond as collateral, the right to receive that interest portion is issued as YLD.

YLD tokens are transferable NFTs compliant with the ERC-721 standard, with each YLD corresponding to a unique position (collateral bucket).

YLD holders can receive interest payments from the protocol based on the passage of time or upon maturity. They can also sell YLD itself to third parties to transfer the yield rights (market trading of YLD facilitates price discovery for the yield).

By separating YLD, USST holders can maintain stable dollar value while retaining the yield that the underlying assets should generate.

STBL (Governance Token)

This is the native token used for governance and value capture across the entire STBL protocol.

STBL holders possess voting rights on critical protocol proposals, enabling them to decide on adding or removing collateral assets, setting risk parameters, allocating treasury assets, and approving upgrades.

Additionally, as an incentive for holding STBL, the design includes buybacks and burns using protocol revenue in the market, as well as reward distributions for STBL staking.

The three tokens are issued and exist simultaneously, each fulfilling distinct roles: providing liquidity for the stable asset (USST), generating returns for the yield asset (YLD), and enabling governance and value circulation for the governance token (STBL). Together, they form the entire protocol’s ecosystem.

For example, when a user locks RWA tokens, USST and YLD are issued. Users can freely utilize USST while earning interest with YLD.

One protocol earns fees and spread income during this process, accumulating them in its treasury for later use in STBL buybacks and community distributions. This cycle links the value of STBL tokens to the protocol’s growth and revenue, providing STBL holders with incentives for sustained ecosystem development.

Characteristics of the Ecosystem

As mentioned above, this covers the overall structure, but the ecosystem contains several detailed features. I will now introduce the main ones.

◼️Price Stabilization Mechanism

To maintain stability, USST is always overcollateralized with sufficient RWA tokens.

For example, when collateralizing an asset valued at $100, the USST issued is capped at approximately 97% of that value ($97 equivalent), with the remaining 3% pooled as a contingency reserve. This pool serves as the primary loss absorption layer, safeguarding the underlying stability of USST even if the collateral asset experiences a principal loss.

Should losses still occur, the protocol’s Loss Reserve Pool will cover the shortfall, minimizing the impact on USST holders.

When collateral assets default or cease interest payments, the position is marked as default within the protocol. Interest accrual ceases, and recovery and liquidation processes are initiated. During this process, assets may be replaced as necessary, and losses are absorbed by the protocol as a whole to maintain the $1 peg of USST.

Additionally, to prevent the USST market price from deviating from the peg, the system is designed to encourage liquidity provision and arbitrage through a mechanism called LAMP (Liquidity and Minting Pool).

For example, if the market price of USST temporarily falls below $1, LAMP will repurchase USST. Conversely, when there is a shortage, dynamic incentive adjustments (such as minting rewards or burn fee adjustments) will be implemented to encourage new issuance with rewards.

◼️Collateral asset

The defining feature of the STBL protocol is its use of high-quality real-world assets (RWAs) as collateral. Specifically, these include U.S. Treasury Bills (T-Bills) and private credit assets.

STBL issues USST by accepting these RWA tokens from users and locking them within a contract, while simultaneously separating the future interest on those assets as YLD.

As a specific method of collaboration, we will whitelist tokenized assets supplied by trusted issuing entities and establish corresponding Vaults within the protocol.

For example, the aforementioned USDY from Ondo Finance is classified as a “T-Bills Vault” and is managed as an asset yielding 4-5% annually, backed by U.S. Treasury bills with maturities ranging from 3 to 12 months.

When users deposit USDY into the Vault, USST equivalent to approximately 97% of the collateral valuation is minted, with the remaining 3% retained within the Vault as a haircut. Subsequently, the Vault contract receives interest payments and redemptions from U.S. Treasury bonds via Ondo (or a partner custodian), distributing these amounts on-chain to the corresponding YLD NFT holders.

STBL’s target RWA assets extend beyond government bonds to include private credit and other private sector assets.

Examples include loans to small and medium-sized enterprises and tokens for resilient financial products, which offer relatively high yields of 10-12% per annum in exchange for some credit risk.

STBL establishes acceptance criteria for each asset through its governance framework, permitting only those with high creditworthiness. The specific approval process involves conducting due diligence on RWA tokens provided by partner institutions—examining legal backing, issuer creditworthiness, market size, and other factors—followed by community voting to add them to the whitelist.

◼️Regulatory compliance

STBL is designed with a strong awareness of financial regulatory requirements. Particular emphasis is placed on KYC/AMLcompliance and securities law treatment.

First, STBL implements whitelist/blacklist functionality at the protocol level. Specifically, addresses capable of minting USST, receiving YLD, or depositing/withdrawing collateral in the Vault are strictly limited to pre-approved wallets only.

To be added to the whitelist, users must pass KYC verification by the operator or affiliated custodian. Only users who have undergone proper identity verification and sanctions list checks can fully utilize the protocol.

Additionally, known malicious addresses (such as those used to receive hacked funds or subject to sanctions) are blacklisted, blocking even token transfers. Governance holds the authority to manage these lists, with additions and removals made through on-chain voting. This mechanism ensures an environment accessible only to users compliant with the law.

◼️STBL Token Allocation

STBL is a utility token responsible for protocol governance and value redistribution. The total issuance cap for STBL is fixed at 10 billion tokens, with approximately 700 million tokens (7% of the total) allocated as the initial circulating supply at the time of the Token Generation Event (TGE) on September 16, 2025.

The remaining tokens will be allocated to various categories such as investors, the team, and the community, and will be gradually released to the market according to specific lock-up and vesting schedules.

Foundation (Finance & Liquidity)

25% of the total supply. This breaks down into 15% for the protocol treasury and 10% for ensuring market liquidity and market making. At the TGE, 45% of the treasury allocation and 4% of the liquidity allocation will be immediately available, with the remainder released linearly over 12 months.Core Development (Team, Advisors, Ecosystem)

A total of 36% is allocated to core development-related activities. The breakdown is 20% for the team, 5% for advisors, and 11% for ecosystem development. Lock-up periods are set for each to encourage long-term commitment. For the team and advisor allocations, a 5% portion is released after a 12-month cliff period following the TGE, with the remainder subject to linear vesting over the subsequent 18 months. The ecosystem development allocation will see 10% immediately assigned at TGE, with the remaining 90% released linearly over 12 months. This ecosystem allocation will fund developer incentives, partnerships, and community development initiatives.Staking rewards

20% is reserved as a reward pool for network staking rewards and security. This portion will be locked for 6 months after the TGE and then released linearly over 18 months, to be used for initial bootstrapping and ongoing staking reward emissions.Private Sale (Investor Allocation)

15% is allocated for early investors. This breaks down to 12% (1.2 billion tokens) for Private Sale 1 (the existing seed round) and 3% (300 million tokens) for Private Sale 2 (an upcoming additional round). In both cases, the tokens are granted with the condition that they are locked for a set period and then gradually released.Community Distribution (Public)

4% is reserved as a public distribution allocation for the community. This is intended to provide tokens to general participants. The distributed tokens will undergo a 3-month cliff period following the TGE, after which they will be released and distributed linearly over the subsequent 6 months.

Furthermore, the STBL token is not merely a governance token; it possesses core utility that returns the protocol’s value to its holders.

The main uses and functions are as follows.

Participation in governance (voting rights)

STBL holders can participate as a community in protocol decision-making. By staking (locking up) tokens, they gain the right to submit proposals and vote, with the weight of their votes increasing the longer the tokens are locked.

Staking and Reward Incentives

By staking STBL tokens, participants can earn rewards from the protocol. Specifically, through a unique mechanism called Multi-Factor Staking (MFS), rewards are designed to be boosted when users lock STBL alone or in pairs such as STBL+USST or STBL+YLD for a set period.

STBL staking rewards are paid from a pool allocated 20% of the total supply, as described above. Additionally, they are distributed using protocol revenue as the source. This structure allows users who hold and lock STBL to directly benefit economically from the protocol’s growth.

Protocol Revenue Distribution (Fee Allocation and Buyback Burn)

The STBL protocol charges issuance and redemption fees for USST, as well as a fixed percentage protocol fee from the interest earned by YLD holders. All these revenues are accumulated in the on-chain treasury and returned to STBL holders in the following ways, based on governance decisions:

① Premium Buyback: The protocol periodically purchases STBL tokens at a price higher than the market rate and immediately burns them to reduce the circulating supply.

② Allocation to staking rewards: Used as the funding source for rewards to staking participants

③ Governance Incentives: Used to encourage voting participation and reward community activities.

◼️Money as a Service(MaaS)

STBL not only issues stablecoins via its own protocol, but also champions a Money as a Service (MaaS) model, providing infrastructure that enables external institutions and ecosystems to issue and operate their own stablecoins.

Specifically, it enables each company, financial institution, government, and other entities to issue their own branded stablecoin (Ecosystem-Specific Stablecoin / ESS) on the STBL platform.

By utilizing the infrastructure provided by STBL, these issuers can programmatically issue their own currencies on a secure, compliant money rail without needing to build a financial system from scratch (similar to how major corporations issue their own credit cards using Visa’s infrastructure).

Additionally, the USST provided by STBL functions as a bridge currency and liquidity hub between each issued ESS. By anchoring all ESS tokens to USST, it ensures global compatibility, enabling each proprietary currency not only to operate within its closed network but also to mutually exchange and settle at a 1:1 value ratio.

Transition and Outlook

As mentioned above, STBL is a next-generation stablecoin protocol dubbed “Stablecoin 2.0,” launched in 2025 by Reeve Collins, co-founder of Tether (USDT), and others.

The background includes the expansion of the stablecoin market in the mid-2020s and the rise of Real-World Assets (RWAs) such as tokenized government bonds. To address the challenges of traditional stablecoins—such as opaque yields, centralized management, price volatility risks associated with pure crypto-asset collateral, and algorithmic instability—STBL proposes a new path (the fourth model). This model utilizes regulated RWA as collateral while returning interest income to users and enabling community governance.

The roadmap outlined broad phases at the TGE in September 2025, followed by the release of specific quarterly plans. Key milestones are as follows:

September 2025:Phase 1– Issuance of STBL tokens and initial listings (Binance Alpha, Kraken). This initiates market trading and establishes the initial community.

Q4 2025:Phase 2– Commencing implementation of the governance framework. Specifically, providing STBL staking contracts and voting UI, and executing initial community proposals. Following security verification, governance will be activated on a limited basis.

Q1 2026:Phase 3– USST mainnet deployment and launch of DeFi lending functionality. Full-scale USST issuance commenced in January (general users began access via whitelist), with enhanced peg monitoring through Hypernative integration. Additionally, a decentralized lending pilot program was initiated.

Q1 2026 (Continued)In February, we will further expand liquidity and broaden the types of RWA collateral (introducing Private Credit, etc.). We will also deploy the Ecosystem-Specific Stablecoin (ESS) framework on the testnet. In March, we plan to natively deploy USST to high-performance chains like Solana and Stellar. Furthermore, we plan to release a simplified DApp interface to enhance usability.

In terms of funding, the project secured capital in its early stages through a pre-seed round led by digital asset management firm Wave Digital Assets. In February 2026, as mentioned earlier, it received strategic investment (treated as a seed round) from OKX Ventures, the venture capital arm of cryptocurrency exchange OKX.

This investment supports STBL’s mission to build a money infrastructure, with OKX expressing its expectation that it will “bring highly capital-efficient products backed by real-world assets to the network.”

The Second Stablecoin Boom Arrives

Finally, we conclude with a summary and analysis.

The classification of stablecoin generations varies by protocol, so here we define the second stablecoin boom according to STBL’s definition.

USDT and USDC gained traction, and from there, Ethena’s USDe rapidly captured attention. During this time, algorithmic stablecoins also existed, alongside crypto-collateralized stablecoins like USDS.

STBL defines Stablecoin 2.0 as encompassing the following elements:

Issued using RWA tokens as collateral

The separation of principal and yield

Governed by a governance token linked to protocol revenue

The ability for companies to create ecosystem-specific stablecoins centered around a core stablecoin

The closest among existing well-known protocols is Ethena. It returns yields on collateral assets, distributes protocol revenue to governance tokens, and supports the issuance of ecosystem stablecoins backed by USDe and USDtb.

STBL is a product that uses RWA collateral and cleanly separates yields.

Personally, I find the approach of extracting only the yield portion as an NFT to be unique. However, since each issuance creates an NFT claim corresponding to that asset, I anticipate that the secondary market will become complex as it fills with assets offering diverse yields and values. Therefore, I suspect that as the secondary market matures, these assets will likely be packaged and consolidated into several financial products.

For example, imagine NFTs or FT tokens being issued that lock NFTs into yet another protocol, granting access to that entire protocol’s revenue. Whether we build this ourselves or a third party does it remains to be seen, but unless we create products that are simple and easy to distribute, the ecosystem will not expand.

Furthermore, as the protocol evolves to integrate all tokens like Money Lego, it becomes inevitable that a default occurring anywhere could trigger the entire ecosystem to collapse instantly.

The most frightening risks are impairment of the value of RWA collateral assets, failure of custodians, and hacking incidents. These risks are fundamentally no different from those associated with USDC or USDT; in fact, one could argue that STBL carries higher risk precisely because it does not hold reserves in fiat currency.

While it may be an acceptable risk once the protocol matures, I’ve recently come to believe that blockchain composability, while expanding possibilities, must not be forgotten for its potential to chain together risks.

That said, as various businesses launch stablecoins within their own ecosystems, the on-chain economy is likely to expand further. I look forward to following the development of these protocols.

That concludes our research on “STBL”!

Reference Links:HP / DOC / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,’‘ we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter “web3 Research” delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.