【SOAR】Providing a mechanism for startups to raise funds without diluting equity by leveraging the DRP standard / @LaunchOnSoar

Could linking unlisted stocks with tokens be the next trend in RWA?

Good morning.

I’m Mitsui, a web3 researcher.

Today I researched “SOAR.”

What is SOAR?

Transition and Outlook

Could linking unlisted stocks with tokens be the next trend in real-world assets?

TL;DR

DRP Standard MechanismSOAR holds a legally binding contract stipulating that during liquidity events, it receives revenue proportional to its issued token ratio (5% issued, 95% unissued). New issuances alter this ratio, increasing or decreasing payment obligations.

Corporate IncentivesAn automatic balancing mechanism that generates revenue through initial funding (5% circulating supply) and transaction fees, but requires token buybacks in the market to reduce payments if desired, as the payment ratio increases with new issuance.

Future OutlookThe linking of tokens to private companies is expected to be the next RWA trend, and SOAR aims to create a more reliable capital market than traditional meme coins through legally binding token issuance by founders who have completed KYC/KYB.

What is SOAR?

SOAR is a decentralized token launchpad operating on the Solana blockchain, providing a mechanism for startups to raise funds without diluting equity.

The defining feature of SOAR is its token standard called DRP (Digital Representation of Participation) (patent pending).

This mechanism differs from conventional ICOs and IEOs and possesses the following characteristics:

Issued TokensOnly 5% of the total supply is automatically deployed to the bonding curve and liquidity pool.

Custodial TokensThe remaining 95% remains unissued and is held in a wallet jointly managed by the founders and SOAR.

Transaction fee2% is allocated, with SOAR and the company each receiving 1%.

3-month lock-up period:No additional issuance is permitted for three months after token issuance and deployment.

72-hour advance noticeNew token issuance after the lock-up period requires a 72-hour prior public notice.

Furthermore, this token standard incorporates a senior debt mechanism.

When issuing tokens via SOAR, a legally binding debt agreement is established between SOAR and the founding company. Upon the occurrence of liquidity events (Series A/B/C funding rounds, EXIT, IPO), SOAR holds the right to receive proceeds proportional to its issued token ratio.

For example, when a company raises ¥1 billion in Series A funding while its issued tokens remain at 5%, ¥50 million (5% of ¥1 billion) is paid to SOAR. SOAR has declared it will return the received funds to token holders in some form. Several methods are explicitly stated, such as airdrops or token buybacks.

So why do companies issue tokens?

This is because it enables fundraising through token issuance and generates revenue from transaction fees. While 5% of newly issued tokens immediately go into liquidity and cannot be used for fundraising, transaction fees are collected. Furthermore, subsequent new issuances allow for fundraising by gradually selling tokens on the market, enabling a fundraising model similar to that of listed companies.

However, as the proportion of new issuances increases, the payment ratio improves during corporate liquidity events (Series A/B/C, EXIT, IPO).

Therefore, when companies wish to reduce payments, they can adjust the ratio of tokens in circulation by purchasing tokens from the market.

It may have gotten a bit complicated, but I’ll now formally explain it again using the terms specified in the documentation.

AUTHORIZED Tokens(AT)Total token supply

ISSUED Tokens(IT)Circulating Supply of Tokens

CUSTODIAL Tokens(CT):SOAR and the amount of tokens held in the custodial wallet under joint corporate management

OUTSTANDING Tokens(QT)The rights and token amounts SOAR is entitled to receive during corporate liquidity events

AT is 100%, and at initial token issuance, IT is 5% and CT is 95%. QT = IT and also AT - CT. Therefore, at initial token issuance, QT = 5%.

Well, it’s the same as what I explained above. The key point is the ratio of IT to CT. If IT increases, token-based fundraising might be possible, but the payment ratio during equity fundraising will rise. Furthermore, unnecessarily increasing the token supply leads to dilution, causing the token price to fall and consequently reducing transaction fee revenue.

Therefore, controlling distribution is difficult and must be done appropriately.

However, as explained so far, while the initial token economics were as described above, the perspective changed slightly in December 2025. The reason is that with 95% of the total supply locked and only 5% circulating, the FDV calculation becomes problematic, making it particularly difficult for beginners to understand.

Going forward, MC will be FDV, and new tokens will be minted rather than transferred from the wallet upon issuance.

Transition and Outlook

SOAR is a project founded in 2025 and based in Wyoming, USA. Building upon Solana’s ICM vision, it aims to create a society where investing in private companies is accessible to everyone.

While launchpads enabling startups to issue tokens have existed in the past, none were legally binding, and most remained within the realm of meme coins.

SOAR builds a system where every startup can issue tokens while adhering to legal constraints, ensuring token holders receive formal value returns.

Furthermore, it points out that an increasing number of startups cannot be fully evaluated solely through funding from existing VCs. As a capital market characterized by quality, accountability, and transparency, it aims to create a platform enabling hardware companies, media companies, and AI companies—which cannot be adequately assessed by traditional VCs—to gain direct access to global retail and institutional investors.

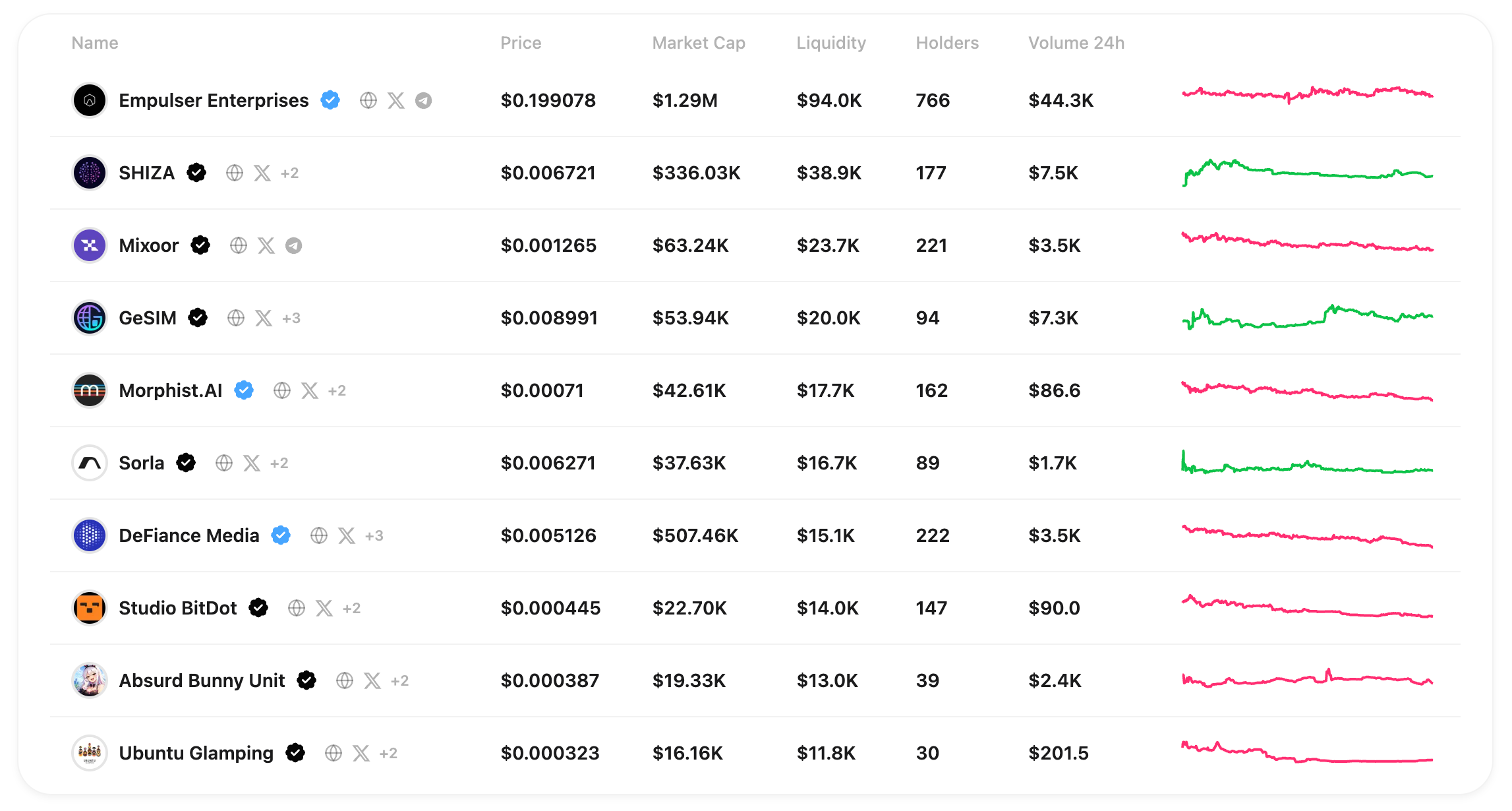

Let’s look at a specific example. Currently, 17 companies are issuing tokens on SOAR.

However, companies also have rankings.

Curated: The SOAR team conducted thorough research and review, confirming strong execution capabilities and credibility in the business model, founders, and team.

Verified: Completed identity and business verification, verified domain, signed DRP launch agreement

Unverified: No identity verification, business verification, or signed DRP agreement

In other words, anyone can be featured, but the quality of their reviews is made visible. However, it is explicitly stated that even if SOAR reviews exist, future success is not guaranteed.

Currently, three companies have been selected for Curated.

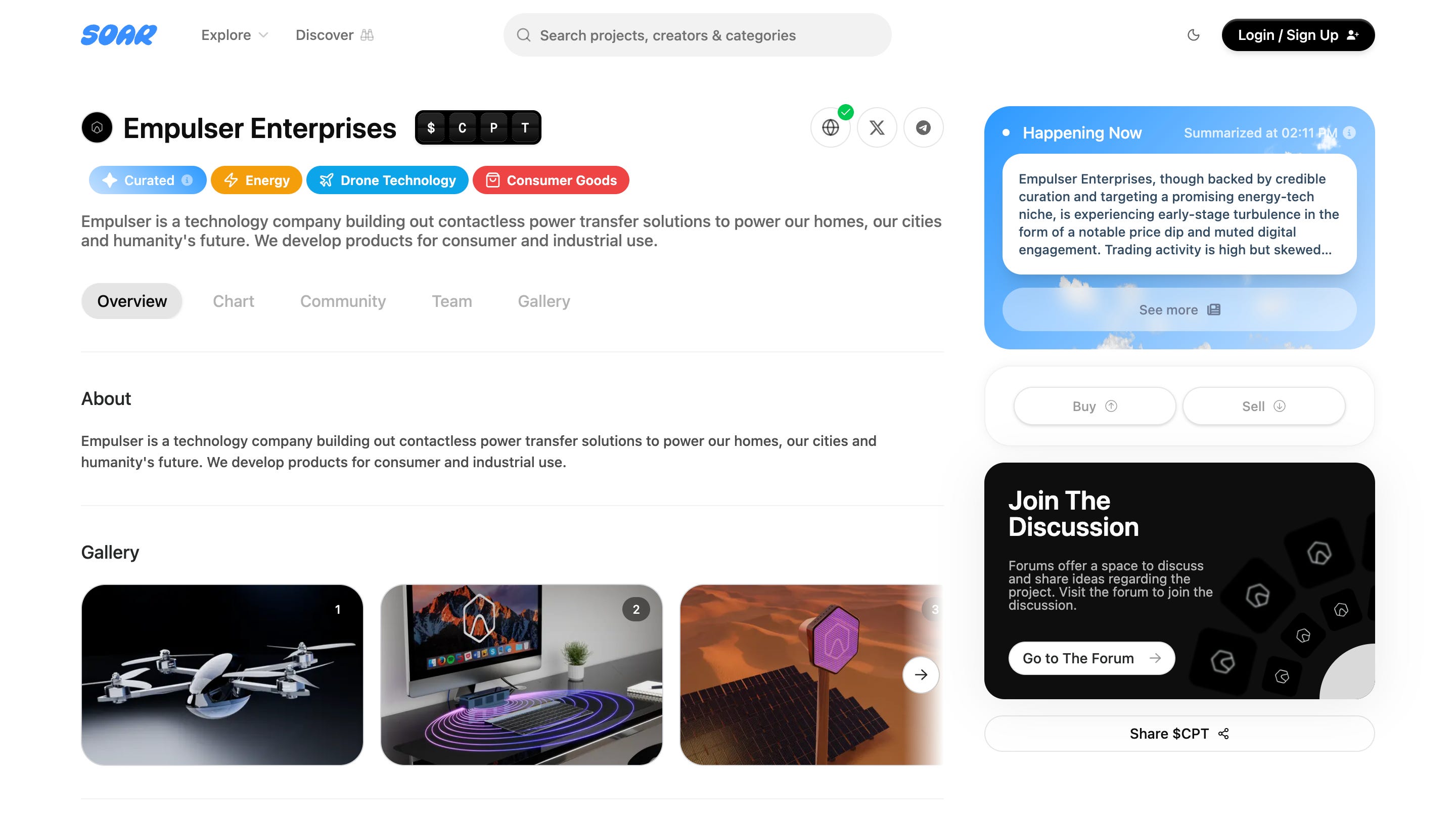

①Impulses

We are a technology company building contactless power transmission solutions that support the future of homes, cities, and humanity, developing products for both consumers and industry.

②DeFiance Media

A new media platform delivering news and entertainment to 80 million households via streaming TV, mobile, desktop, and satellite broadcasts, focusing on open finance, digital assets, and the future of DeFi.

③Morphist.ai

Developing the ultimate multi-model AI platform that runs locally, unifying every model, every query, and every response through a sophisticated interface. Seamlessly switch between any AI model in real time, maintain conversation privacy, and ensure complete data sovereignty.

Moving forward, all companies will utilize it, and improvements toward realizing ICM are expected to continue.

Could linking unlisted stocks with tokens be the next trend in RWA?

Finally, we conclude with a summary and analysis.

Personally, I believe linking unlisted stocks (startups) with tokens will become the next trend in Real-World Assets (RWA), and I’m keeping a close eye on it. The reasons are the enormous market size of unlisted stocks and the fact that AI advancements now enable teams of one or just a few people to build global services.

Going forward, I believe we’ll see more startups developing services with small teams using AI and raising funds globally through blockchain. While the ultimate exit will likely return to equity, tokens may be utilized during the initial launch phase.

Of course, if anyone can issue tokens to raise funds, fraudulent tokens will proliferate. And even if it wasn’t intentional fraud, startups are more likely to fail, so token holders are also highly likely to suffer losses.

However, tokens issued by individuals who have undergone KYC/KYB verification linked to stocks are certainly more reliable than mere meme coins. This is because the issuance costs are high.

The SOAR we researched this time uniquely links shares and tokens. While it’s interesting that it imposes legally binding obligations on startups, the aspect of attaching payment obligations during fundraising is particularly intriguing. Although SOAR acts as an intermediary until returns are distributed to token holders, my personal prediction is that fully automating this process would constitute a security, making it legally impossible from a regulatory standpoint.

That said, the mechanism of growing a startup while controlling token circulation is extremely interesting, and I expect it could become a new form of corporate management.

Of course, I don’t expect all stocks to suddenly become tokens overnight. First, we’ll see the emergence of mechanisms where a portion of stocks—linked to corporate activities like equity financing and sales—are converted into tokens under legal contracts that return value. This marks the beginning of an era where we test whether such systems can function effectively.

Several interesting projects have been emerging, so I’m personally keeping track of them while also hoping to compile a report on them at some point!

That concludes our research on SOAR!

Official Link:HP / DOC / APP / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,'' we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter "web3 Research" delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.