【Polaris】Aiming for a Fully Decentralized Stablecoin Issuance Infrastructure with a 3-Token Model / @polarisfinance_

Can it become DeFi's "last line of defense"?

Good morning.

I’m Mitsui, a web3 researcher.

Today I researched Polaris Finance.

Beginning as a Tomb fork on the Aurora chain, it is now a project on Ethereum with the vision of a “Stablecoin OS.” While the token mechanics may seem complex, we’ve summarized everything from its evolution to the new protocol’s structure, so please read through to the end.

What is Polaris Finance?

New Polaris Protocol

Team Ecosystem: Future Outlook

Can it become DeFi’s “last line of defense”?

Thread; Long story short

Polaris was born in 2022 as a fork of Tomb Finance on the Aurora chain. Starting with an algorithmic stablecoin pegged to NEAR, it expanded into a multi-peg system capable of issuing up to seven different pegged currencies.

In Phase 2, we built PolarEX, our proprietary DEX based on Balancer V2, and launched it on both Aurora and Telos chains. We also introduced vote-escrow governance (veXPOLAR).

However, due to the structural challenges (death spiral) of the entire Tomb-style fork ecosystem, TVL has decreased by over 99% from its peak. The POLAR token also plummeted from $219 to nearly $0.

By the end of 2025, the team announced it was developing a completely new CDP-type stablecoin protocol, “Polaris Protocol,” on Ethereum. It features a three-token model: pETH (ETH derivative), pUSD (yield-bearing stablecoin), and POLAR (governance token), characterized by immutable code design. Notable DeFi analyst TokenBrice joined as a co-founder.

What is Polaris?

Polaris is a stablecoin-focused protocol in the DeFi space.

Originally launched in February 2022 on the Aurora Chain (NEAR’s EVM layer) as a fork of Tomb Finance.

First, to understand the evolution of this project, we’ll start by organizing the background.

◼️Why the Tomb Finance Fork?

From 2021 to 2022, a project called “Tomb Finance” garnered significant attention within the DeFi community. Tomb Finance is a protocol operating on the Fantom chain that issues “TOMB,” an algorithmic stablecoin pegged to FTM.

The mechanism was simple: it used three tokens—stablecoin, share token, and bond token—to maintain the peg by balancing supply and demand. At one point, its TVL exceeded $1 billion, and over 100 forks were deployed across various chains worldwide.

Polaris Finance emerged as the first Tomb fork on Aurora. What sets it apart from other forks is its approach of “multi-peg” rather than a single pegged currency—that is, integrating and managing multiple assets pegged to different assets under a single governance token.

◼️Phase 1: Multi-Peg Signorage Model (2022)

In the initial phase of Polaris Finance, we adopted a seigniorage model consisting of the following three types of tokens.

$POLAR:An algorithmic stablecoin pegged to NEAR. Its mechanism involves new issuance when the price exceeds the peg and a reduction in supply when it falls below.

$SPOLAR:Governance & Share Token. With a fixed maximum supply of 50,001 tokens, staking them in a contract called the “Boardroom” allowed holders to receive POLAR expansion rewards (80% of newly issued tokens).

$PBOND:Bond Token. Issued when the POLAR price falls below the peg. Users burn POLAR to purchase PBOND at a discount, which is redeemed at a premium once the peg is restored. This mechanism served to assist in price stabilization.

A key feature is that Polaris didn’t limit this model to a single pegged currency. Starting with POLAR pegged to NEAR, it expanded to include seven pegged currencies in total: “ETHERNAL” pegged to ETH, “ORBITAL” pegged to BTC, “USP” pegged to USDC, and even “BINARIS” pegged to BNB. The design integrated the reward distribution for all these pegged currencies under a single SPOLAR token.

However, the LUNA peg’s “LUNAR” was excluded due to the Terra/LUNA collapse in May 2022, demonstrating significant susceptibility to external environmental factors.

◼️Phase 2: Building a Balancer V2-based DEX (2023–2024)

As the limitations of the Signoraggio model begin to emerge, the team will embark on Phase 2: building its own DEX, “PolarEX.”

PolarEX is built on Balancer V2’s AMM technology, enabling advanced liquidity provision such as weighted multi-token pools and stablecoin-to-stablecoin stable swap pools. For example, it combines USDC, USDT, and their respective bridge versions into a single Composable Stable Pool, achieving low-slippage trading.

New tokens were also introduced in this phase.

$xPOLAR:DEX-exclusive incentive token (maximum supply of 4 million, halving every two years).

$veXPOLARA:Curve-style vote-escrow token. Obtained by locking SPOLAR, xPOLAR, or NEAR LP tokens, it grants the right to vote on the distribution of liquidity rewards on the DEX.

Furthermore, PolarEX has expanded to the Telos chain by leveraging LayerZero technology, achieving multi-chain deployment beyond Aurora.

◼️Structural Collapse of the Tomb Fork

However, Tomb-based forks including Polaris Finance could not escape their structural challenges.

The greatest weakness of the Signoraggio-type algorithmic stablecoin is its dependence on new capital inflows. As long as buying pressure persists, it trades above the peg, boardroom rewards are generated, demand for share tokens increases, and a positive spiral takes hold.

However, once capital inflows cease, it falls into a “death spiral”: peg breakdown → reward suspension → share token sales → further peg breakdown.

As a result, the POLAR token fell from its launch-day peak of approximately $219 to $0.03 by 2024. CoinMarketCap currently lists it at nearly $0, with a daily trading volume also recorded as $0. SPOLAR is similarly in a suspended trading state. According to DefiLlama, the protocol’s TVL is approximately $79,000 on Aurora and $216 on Telos, effectively close to zero.

This is not a problem specific to Polaris.

Tomb Finance itself, the original fork, saw its TVL collapse from $1 billion to approximately $78,000, and nearly all of its 12 chains and over 104 forks met the same fate. This serves as an industry-wide lesson demonstrating how difficult it is to achieve lasting price stability through algorithms alone.

New Polaris Protocol

By the end of 2025, the Polarisfinance website underwent a complete overhaul and was reborn as an entirely new project: “Polaris Protocol – Self-Scaling Stablecoin Operating System.”

Building on the lessons learned from the previous protocol’s failures, the design has now shifted away from relying solely on the algorithm. Instead, it centers on a Collateralized Debt Position (CDP) model backed by ETH as collateral.

This might be a bit complicated, but I’ll explain it as clearly as possible.

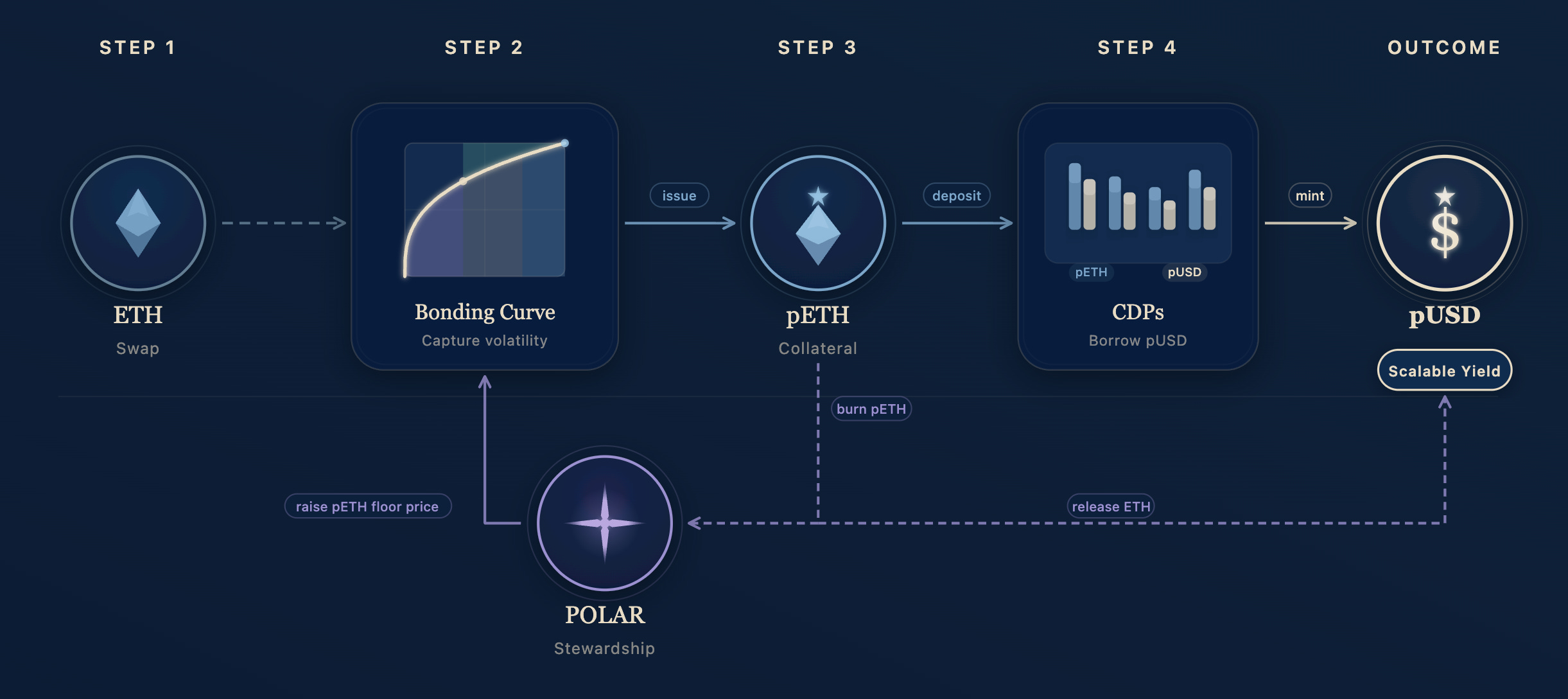

◼️New Tokenomics: pETH / pUSD / POLAR

The new Polaris Protocol adopts a three-token structure known as the “Triple Engine Model.” However, its roles and design philosophy are entirely different from the previous model.

$pETH:ETH Derivative Token

Issued when users deposit ETH into Polaris’s “bonding curve.” Unlike typical AMMs, the issuance price is determined along a mathematically defined curve, so pETH always has a rising floor price (lower limit).

The key point is that as protocol activity increases, the ETH backing per pETH token grows, making pETH an asset with greater value than ETH itself. pETH is designed to function as a yield-bearing asset.

$pUSD:Interest-bearing stablecoin

pETH is a USD-pegged stablecoin issued via the CDP mechanism using pETH as collateral. It’s the same concept as borrowing DAI or LUSD from MakerDAO or Liquity.

A key feature is that pUSD will incorporate a mechanism that generates yield simply by holding it. The sources of yield are all on-chain revenues completed within the protocol, including borrowing interest, swap fees from the bonding curve, conversion gains to POLAR, and DEX trading fees.

$POLAR:Stewardship (Management) Token

The most significant feature of the new POLAR lies in its issuance mechanism. POLAR is a one-way conversion process that can only be minted by burning pETH.

What makes this mechanism interesting is that each time POLAR is issued, the supply of pETH decreases, causing the ETH backing (floor price) per remaining pETH to rise. In other words, POLAR issuance drives up the value of pETH, which in turn enhances the collateral safety of pUSD, creating a positive feedback loop.

POLAR holders are entitled to receive real yields from the protocol and can participate in governance voting and incentive distribution by locking their tokens to convert them into vePOLAR.

◼️Peg Maintenance Mechanism: Redemption and Minting

In the traditional Signoraggio model, maintaining the peg relied almost entirely on algorithmic supply adjustments. The new Polaris introduces a market arbitrage mechanism similar to Liquity.

pUSD is less than $1 (decoupling):Arbitrageurs purchase pUSD cheaply in the market, redeem it with the protocol to receive $1 worth of pETH, and then sell it. This supports the pUSD price.

pUSD > $1 (Peg Deviation):Arbitrageurs add pETH as collateral, mint new pUSD from the system, and sell it on the market. This increases supply and lowers the price.

What’s even more interesting is the automatic interest rate adjustment mechanism. When pUSD deviates below the peg, borrowing rates automatically rise to encourage repayment. Conversely, when pUSD deviates above the peg, rates decrease to incentivize borrowing. This design philosophy minimizes reliance on external price oracles, instead performing feedback control solely using internal system information.

◼️Stablecoin OS: A platform enabling anyone to issue stablecoins

And Polaris has an even greater vision: the “Stablecoin OS.”

This is a platform that tokenizes any “unit of value”—from pUSD to pGOLD (gold-pegged), pCHF (Swiss franc-pegged), pEUR (euro-pegged), and even assets linked to the Big Mac Index—all while using pETH as common collateral.

Since all pegged assets share a single pETH pool as collateral, even if pGOLD liquidations occur due to sudden gold price fluctuations, pUSD and pCHF remain largely unaffected. This structure ensures that while some branches may shake, the trunk (collateral pool) remains sound.

External projects require approval from vePOLAR holders to utilize this infrastructure, and adopted projects will return a portion of their revenue to the Polaris ecosystem. An incentive structure similar to Curve’s ve war could emerge, centered around voting rights.

Team Ecosystem: Future Outlook

◼️Team: TokenBrice Participation

The initial Polaris team operated anonymously, but starting in late 2025, two individuals stepped forward as co-founders of the new protocol.

TokenBrice:He is a prominent analyst/writer in the DeFi space, known for his incisive insights shared on the blog “Brutally Honest DeFi.” He also has a background as a consultant for Liquity. Concerned about the current trend of decentralized stablecoins becoming centralized, he joined as a co-founder of Polaris.

Robert Mullins (0xBones):A Solidity developer with over 7 years of stablecoin development experience. Serves as the technical lead.

TokenBrice has stated it aims to reach a 10-digit supply (worth billions of dollars) within two years, setting an extremely ambitious goal. VC funding has not been publicly disclosed, and the project is positioned as community-driven.

◼️Governance: The concept of “stewardship”

The new Polaris governance system is called “Stewardship,” a design that sets it apart from conventional DAO governance.

This is a restricted governance model where “authority exists to adapt and evolve the protocol, but not to alter its core essence.” The core smart contract is immutable after deployment, with no administrator keys or backdoors.

vePOLAR holders can only adjust parameters (interest rates, liquidation fee rates, incentive amounts, etc.) within the predefined range permitted by the code. Moreover, changes require voting + a time lock and do not take effect immediately.

For instance, changes that violate Polaris’s core principles—such as “adding USDC as collateral”—cannot be put to a vote at all. This design systematically prevents situations like the one that actually occurred in MakerDAO, where a governance vote introduced a centralized asset.

◼️Roadmap

TokenBrice stated, “The protocol has not launched yet. This is not a product announcement, but a sharing of our commitment,” giving the impression of proceeding cautiously with preparations. A mainnet launch is anticipated sometime in 2026, though a specific date has not been announced.

Can it become DeFi’s “last line of defense”?

Finally, we conclude with a summary and analysis.

Polaris Finance is a project that has undergone a highly unique evolution.

Phase 1, as the first Tomb fork, collapsed alongside the structural limitations of algorithmic stablecoins as a whole. While this was a failure, it also provided the team with a firsthand opportunity to learn “what went wrong.”

The new Polaris Protocol is a completely different approach based on those lessons. With its ETH-collateralized CDP model, floor price mechanism via bonding curve, on-chain yield structure, and governance restrictions via immutable code, Polaris is determined to remain “zero off-chain dependency” while USDC and Ethena steer toward reliance on government bonds and centralized exchanges.

Polaris proclaims itself the “North Star of DeFi” and the “last line of defense,” and I’m very excited to see how far its decentralization challenge will grow.

That said, while many such projects have emerged in the past, none have significantly eroded the market share of existing stablecoins. I’m eager to see what strategy they’ll employ to gain traction.

Without simple yields and diverse use cases on DeFi, I don’t think it will gain traction. I’m looking forward to seeing what kind of yields dollar-pegged stablecoins will offer.

First, I’d like to wait for the mainnet launch.

That concludes our research on “Polaris”!

Reference Links:HP / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,'' we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter "web3 Research" delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.