【Payy】Privacy-focused on-chain bank with a focus on stable coin / Offers privacy-protected transactions through its proprietary ZK roll-up chain, Payy Network / @payy_link

Provides anonymity for everyday transactions.

Good morning.

I am mitsui, a web3 researcher.

Today I researched "Payy".

🏦What is Payy?

🚩 Transition and Prospects

💬Birth of the Stable Coin Bank

🧵TL;DR

Payy is a USDC-centric on-chain bank that provides privacy-protected transactions through a self-managed wallet and its own ZK roll-up chain, the Payy Network.

Key features include linked money transfers (via ephemeral wallets), zero-commission money transfers, bank on/off ramps in the US and Argentina, and Visa debit card payments.

It is not completely anonymous, but features "compliant privacy" that meets regulatory requirements through UTXO genealogy tracking and "proof of innocence," while keeping transaction details confidential.

🏦What is Payy?

Payy" is an on-chain banking platform with a focus on stable coins.

The main function is a non-custodial wallet that allows users to self-manage their own assets, and transactions such as money transfers are designed to run on a proprietary blockchain (Payy Network) with privacy protection features.

In particular, the goal is to develop various use cases for utilizing stablecoins in traditional financial areas such as payroll, outsourcing payments, royalty distribution, trade finance, etc. by providing privacy to the issue of all on-chain transaction history being publicly available. The company aims to develop various use cases for stablecoin in traditional financial areas such as payroll, outsourcing payments, royalty distribution, and trade finance.

In the following section, we will explain its characteristics.

◼️Payy Wallet

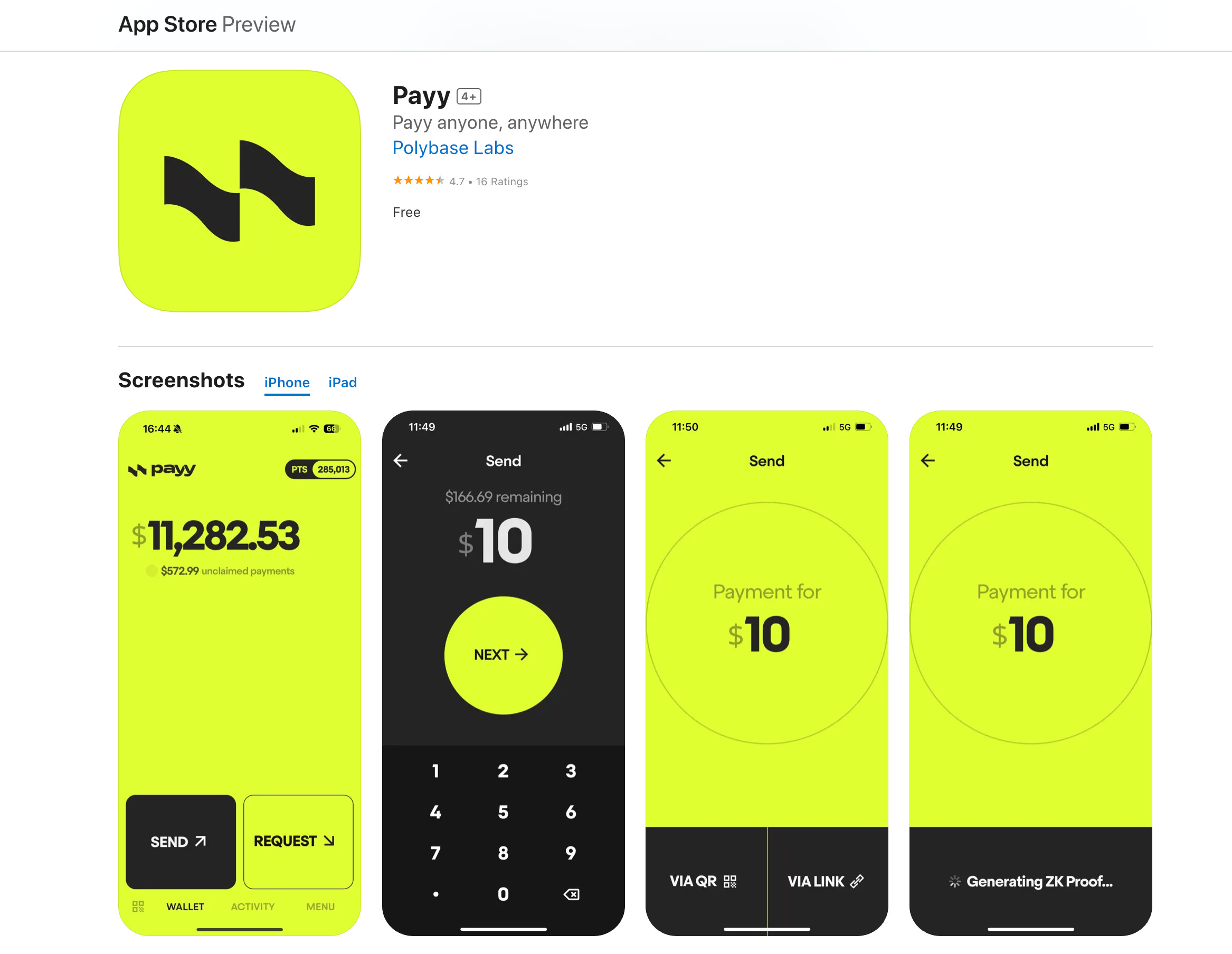

Currently, IOS and Andoroid apps are available, and a non-custodial wallet is generated by registering for an account when using the apps.

A key feature is that it is an on-chain banking platform that is based on stablecoin, which means that balances stored in Payy Wallet are basically represented in USDC.

When assets from other chains, not just USDC, are transferred, they are bridged to USDC on its own Payy Network chain.

As of 2025, bank-connected deposits are available in the U.S. (USD) and Argentina (ARS) (U.S. is in beta). For example, U.S. users can transfer dollars using ACH account transfers within the app and immediately receive USDC equivalent to the amount transferred as their Wallet balance, and vice versa. The reverse is also true.

The primary currency available as of 2025 is the U.S. dollar stave coin, although expanded support for other currency-denominated stave coins (e.g., euro-linked) has been suggested in the future.

In addition, all transactions (transfers and payments) on Payy are commission-free for users. This is made possible by the fact that Payy aggregates transactions on its own chain, and the chain operator handles and absorbs the roll-up costs to L1 and bridge fees internally.

◼️Payy Network

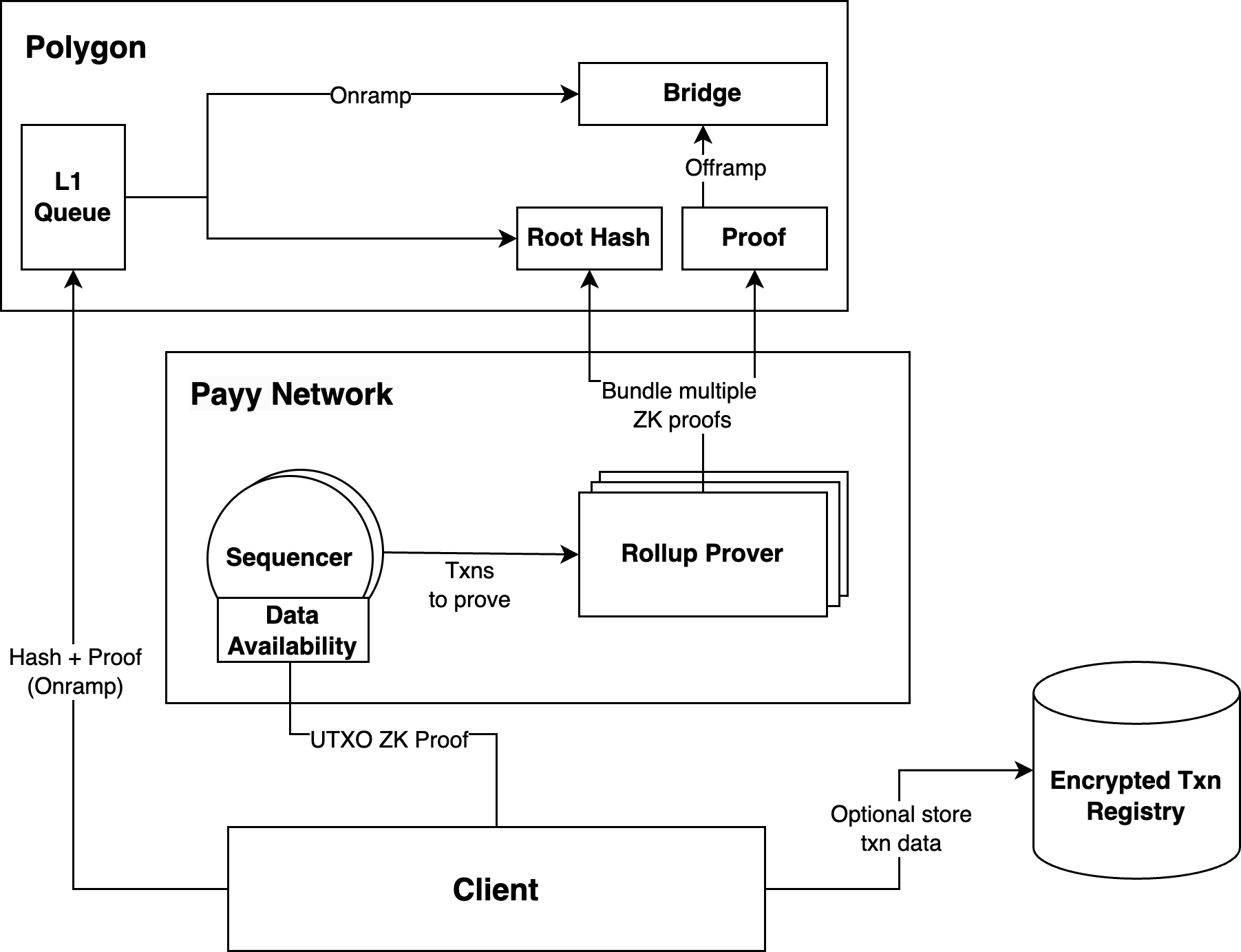

Payy is building its own blockchain, the Payy Network.

The Payy Network is an L2 built on top of the Ethereum ecosystem and is designed to balance privacy and compliance. Specifically, it is a Validium-style ZK rollup that relies on the Ethereum mainnet (and currently the Polygon network) for security, while transaction data is processed off-chain.

On this network, transaction details are recorded as cryptographic commitments (hashes), and the entire network state can be updated without exposing real data.

(This is a detailed technical discussion, so you can skip this part.)

Payy Network's consensus is operated by a network of sequencers based on Proof of Stake, with an algorithm called HotStuff to achieve immediacy of about 1 second.

The correctness of the final block is verified by a zero-knowledge proof (ZK-SNARK), and the corresponding hash is periodically written to the L1 blockchain to ensure security and irreversibility.

With this architecture, Payy combines the scalability of a proprietary chain with the security of Ethereum. Payy is also unique in that it is not EVM-compatible and has a custom-designed ZK circuit built from the ground up to achieve privacy. This means that general-purpose smart contracts are not currently supported, but the structure is focused on transaction processing efficiency and confidentiality.

Payy Network also uses the UTXO (unused transaction output) model rather than an account model like Ethereum.

The advantage of taking the UTXO model is the flexible combination of anonymity and traceability.

Payy calls this "UTXO lineage," and it is designed to meet regulatory requirements, such as anti-money laundering, by allowing only the origin of funds to be verified while keeping transaction details confidential. This is called "UTXO lineage" and is designed to meet anti-money laundering and other regulatory requirements.

◼️EphemeralWallet

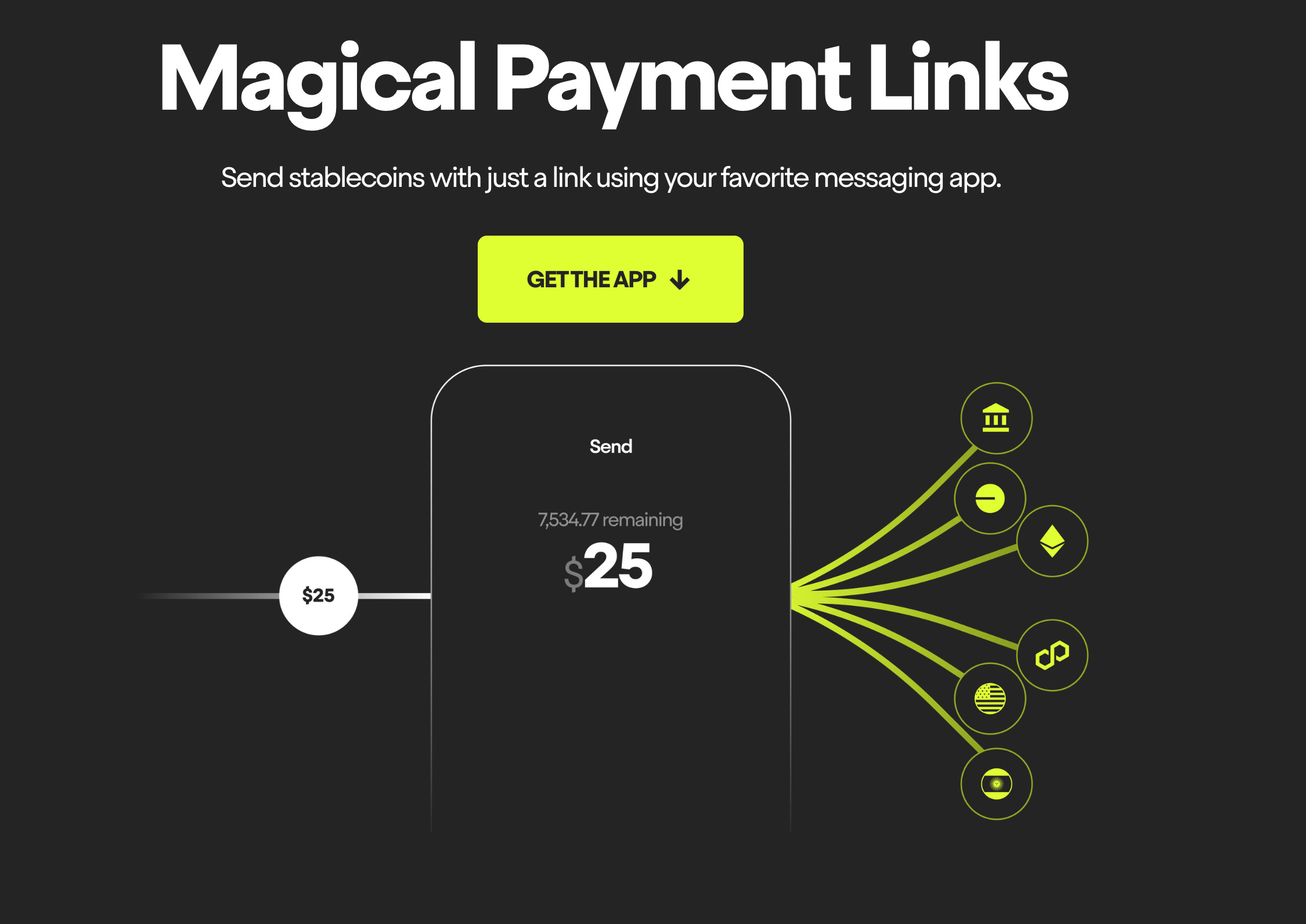

Payy's unique privacy mechanism is an ephemeral wallet for linked money transfers.

When a user transfers funds via a "Payy link" or QR code, funds are transferred from his/her wallet to a newly generated ephemeral wallet once it is created.

The private key for this ephemeral wallet is embedded in the link itself, and when the recipient opens the link, the funds are transferred from the ephemeral wallet to the recipient's wallet.

This ensures that no direct on-chain trace remains between the sender and receiver addresses, and that even non-blockchain users can intuitively receive funds through the money transfer link.

◼️Payy Card

Payy offers users a Visa-branded debit card, which was launched in August 2025 as the "world's first on-chain Visa card."

The Payy Card allows users to convert USDC in their own Payy Wallet in real time, enabling privacy-protected payments at Visa merchants.

When paying with a card, the terminal processes a normal Visa transaction, but behind the scenes, USDC equivalent to the purchase amount is instantly debited from the user's wallet on the Payy Network, and the card issuer's (Payy's) account is cleared to pay the merchant.

Again, ZK proof is utilized in this process, and the amount of the transaction tapped and settled is not exposed on the public chain. In other words, the card transaction amount is kept secret on the chain, and even if the Payy Network is monitored by a blockchain explorer, it is not possible to track individual card transactions.

This eliminates the risk that anyone can track on-chain transactions, which many existing "cryptocards" had.

Payy Card's fees are very simple: there are no card issuance fees, no annual fees, and no transaction fees. Basically, users pay in U.S. dollars with no foreign exchange fees, but Payy informs users that a 1% foreign exchange conversion fee will be charged only when paying in foreign currencies (this is expected to be a monetization point for the Payy project). (This is expected to be a monetization point for the Payy project.)

To obtain a card, you can apply for a card online from within the Payy Wallet application, and all you need is an ID and a KYC to confirm your address, and no credit check is required. Once approved, a virtual card is issued instantly and can be used immediately by registering it with Apple Pay or Google Pay.

Physical cards will also be issued to those who wish to receive them, but these are Payy's "light-up cards," a limited edition design with a gimmick that causes the card's logo to glow when used. This physical card is not immediate, but can be applied for after accumulating 100,000 points in Payy's rewards system, Payy Points.

◼️Payy Points

As of August 2025, Payy does not issue platform-specific tokens. Instead, a loyalty program exists.

Payy Points are awarded based on user usage and are operated on a seasonal basis.

Season 1 (Balance Points) began in March 2024 and continued through August 2025; during this period, one point was earned per day for every US dollar in wallet balance.

This means, for example, that if you deposit 1000 USDC in Payy and hold it for one week, you will earn 7,000 points. There is also an invite-a-friend bonus, where you can earn 10,000 points per person if someone else issues a Payy Card at your invitation.

Points earned can be viewed and managed on the app's Rewards page, and are used, for example, to obtain the aforementioned light-up physics card (unlocked at 100,000 points), and various rewards and campaign participation using points are planned for the future.

In addition, the new season will also see the launch of a "Pay to Earn" program that will allow customers to earn one point for every dollar spent on their cards.

It is unclear if this will become a token in the future, but it is a rewards program that will provide benefits within the ecosystem.

🚩Transition and Outlook

Payy is developed and operated by Polybase Labs, a blockchain company originally founded in 2022 by the team behind the "Polybase" distributed database project (database for web3). Polybase Labs was founded in 2022.

This was followed by the development of the Payy Network and Payy Wallet as we focused on on-chain privacy and ZK technology.

The co-founders are Sid Gandhi and Calum Moore, Sid is a software engineer from Apple who has worked as an iOS engineer developing products for millions of users. Calum has released large scale projects for Virgin Media in the UK and has contributed to several blockchain projects in the crypto industry, including ZK Bench and Polybase DB.

They say they got into entrepreneurship out of a sense of challenge that "many blockchain projects have emerged since Bitcoin's introduction in 2009, but their impact on the real world has been scant." Sid specifically states that "it is irresponsible and unethical to offer users a service where all transactions are publicly available. It is borderline from a GDPR perspective," he said, indicating a strong awareness of the urgent need to protect the privacy of financial transactions. This is where the idea for Payy was born.

Payy (Polybase Labs) is funded by prominent venture capitalists and investors. Specifically, Robot Ventures, DBA Crypto, 6th Man Ventures, Orange DAO, and Protocol Labs are among the investors.

💬Birth of the StableCoin Bank

The final section is a summary and discussion.

There are many wallet products that focus on stable coins in terms of current trends, but Payy was unique in several ways.

The first and greatest feature is the anonymity provided by the proprietary chain. It is not realistic to expect all transaction history to be publicly available when really considering general use. When you send money to a friend, you know your friend's wallet address, and you cannot safely use it on a daily basis in a situation where you can see all the information about your account status and past information.

So, the fact that stable coins can be sent to each other while that is kept secret and that payment can be made with credit cards makes a lot of sense in terms of dissemination.

And because it is not completely anonymous, but rather adopts a compliance-conscious form of anonymity, it stands slightly apart from similar anonymous/confidential projects. This is also one of the main characteristics of this project.

Another thing I personally like is that you can't hold all assets, but only one USDC. I think this is partly because it needs to be bridged on its own chain, but it makes sense because when you think of it as an alternative to a bank account rather than an extension of a wallet, you normally don't see assets that are not legal tender.

So Payy can make it possible to keep the same banking experience that we have today.

However, if it doesn't change, there is no need to migrate, so I expect that there will probably be a DeFi operational feature in the future, such as some kind of reward for just holding USDC.

There may be benefits for the store side, such as lower international transfer fees, instantaneous transfers to merchants and lower fees, but these are meaningless to the user, so a clear user benefit needs to be put forth to replace the bank account.

We believe that the easy way to understand this is to put forth a concept like interest rates and say that USDC will give you a 4% interest rate, which is a reward that has advantages when compared to bank interest rates.

Coinbase and other banks have already started this area, and I think that stable coin banks will start one after another, and eventually existing banks will be forced to respond, and the entire financial system will be centered on stable coins.

In this context, I thought it was an interesting project because the ability to send and receive money anonymously, which Payy is taking, is absolutely necessary.

This is the research for "Payy"!

🔗Reference Link:HP / DOC / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,'' we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter "web3 Research" delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.