【Cork Protocol】A programmable risk layer for on-chain assets / Provides insurance against depeg risk / @Corkprotocol

The variety of on-chain insurance products is expanding

Good morning.

I’m Mitsui, a web3 researcher.

Today I researched the “Cork Protocol.”

What is the Cork Protocol?

Detailed mechanism

Transition and Outlook

The variety of on-chain insurance products is expanding

TL;DR

Cork Protocol is a DeFi protocol that provides a “risk insurance market” enabling on-chain pricing and hedging of depeg risks for pegged assets. At its core is Depeg Swap, similar to a CDS, which decomposes risk into tradable forms.

The mechanism involves depositing collateral assets to issue cPT (insurance underwriter) and cST (insurance user), enabling the withdrawal of collateral assets using cST plus pegged assets. This structure simultaneously provides insurance during depegging and premium income during normal periods.

Founded in 2024, the company launched its beta version after being selected by a16z CSX. Following a hacking incident, it was rebuilt as the Phoenix version. It is now collaborating with Lido and Ethena while aiming for full-scale operation as an on-chain insurance infrastructure.

What is the Cork Protocol?

The Cork Protocol is a platform enabling risk pricing and hedging transactions in the DeFi space.

Specifically, we offer “Depeg Swap,” an on-chain financial instrument similar to traditional credit default swaps (CDS), targeting the “de-pegging risk” of pegged assets such as stablecoins and staking tokens.

Cork aims to introduce competitive market functions into areas where price fluctuation risks could not previously be adequately assessed and hedged, thereby achieving stable liquidity and efficient risk management.

We’ll explain the details later, but Cork provides solutions such as the following:

① Peg Resilience

Solutions for stablecoin issuers and liquid staking providers that help maintain price pegs. Even if the peg temporarily breaks due to black swan events, Cork’s programmable risk layer provides defense.

② On-Demand Liquidity

Yearn’s vaults and cross-chain bridges provide liquidity buffers that instantly respond to sudden large-scale withdrawal (redemption) demands for high-yield vault operators. Cork constructs a custom swap market (Cork Pool). Liquidity providers (LPs) deposit liquid assets like ETH or USDC, while vault operators purchase Cork swap tokens. This mechanism establishes an auxiliary liquidity rail for vaults, enabling instant cash conversion.

This enables us to balance revenue generation with reliability assurance—ensuring that even high-utilization vaults can process user withdrawal requests without delay, while also allowing the bridge to safely increase its utilization rate.

③Composite Yield

For liquidity providers on the risk-taking side, we offer a new yield-generating mechanism combining multiple revenue streams: “underlying asset yield + risk premium + Cork incentive.”

For example, when users deposit staked assets (such as stETH) as collateral into Cork, they continue to earn the original staking rewards (native yield) while also receiving premium income as compensation for assuming peg risk and other liabilities, plus additional incentives from the protocol.

This compounding profit structure of “principal yield plus insurance premium income” allows LPs to enjoy a higher composite yield than usual in exchange for assuming risk.

④Protected Loops

We support issuers and managers of RWA and illiquid long-term assets in implementing secure loop strategies (leveraged operations). Typically, looping assets with low market liquidity as collateral makes liquidation difficult. Cork combines a “Loop Vault” with “Cork Pool’s permanent exit option (immediate cash conversion via swap tokens)” to provide a mechanism enabling positions to be instantly unwound, re-collateralized, or liquidated as needed.

This enables multiple rounds of leveraged operations (loops) while hedging liquidity risk, even for long-term assets like real estate collateral that were traditionally difficult to operate in a loop.

As described above, Cork is a platform that can be described as an “on-chain version of the risk insurance market,” serving as a versatile risk management infrastructure applicable to multiple use cases—from depeg insurance for pegged assets to liquidity backstops.

These features enable stable asset issuers to obtain standardized risk pricing metrics for proactive risk management, while also creating a market where investors earn premium income in exchange for assuming risk. This is expected to enhance the stability and efficiency of the entire DeFi ecosystem.

Detailed Mechanism

Now, let’s explain the mechanism in greater detail. While we introduced ① to ④ above, Cork’s main focus is primarily on providing “Depeg Swap” against depeg risk, as seen in ① and ③. Therefore, we will now provide a detailed explanation of that.

◼️Summary

Depeg Swap is a tokenized insurance product that enables the buying and selling of protection against the risk of a target asset’s peg collapse (de-peg).

Similar to traditional financial CDS (credit default swaps), this mechanism transfers the risk of a collapse in an asset’s creditworthiness (in this case, its price peg) to another party. Depeg Swap purchasers pay a certain premium to receive compensation in the event of a depeg, while the underwriter (insurance seller) receives the premium but assumes the position of bearing the loss if a depeg occurs.

In this respect, it is functionally similar to CDS, but differs in that the targeted risk is a breakdown of the pegged price rather than default, and that it is automatically executed and settled on a smart contract.

In particular, Cork’s Depeg Swap is always fully backed by collateral assets, offering the advantage of eliminating the need to worry about counterparty credit risk, unlike traditional CDS.

◼️Mechanism

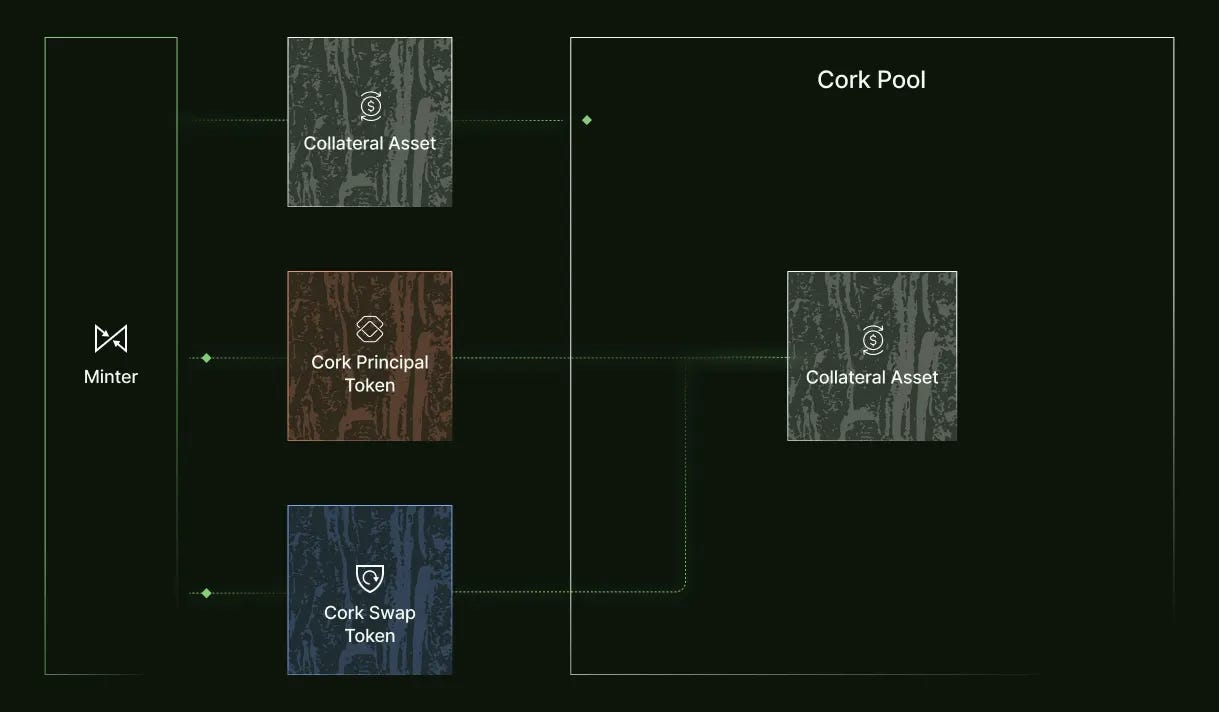

At the core of the Cork Protocol is a smart contract called the Cork Pool, where depeg insurance issuance and liquidation take place.

First, liquidity providers (LPs) deposit collateral assets into the Cork Pool. Collateral assets are the base assets for the depeg insurance, such as ETH or USDC.

Depositing Collateral Assets mints “Cork Principal Token (cPT)” and “Cork Swap Token (cST)” respectively. cPT is a token for pool underwriters, carrying risk instead of yield. cST is a token granting exchange rights during insurance claims or depeg events.

Separately, there exist assets known as “Reference Assets” that can be depegged. Examples include LSTs such as stETH and stablecoins like USDC.

Cork is essentially insurance against depegging, so the sequence is as follows: first, the “Reference Asset (RA)” is determined, then a pool is created for that RA, and finally the Collateral Asset and cPT and cST issuance are carried out. Therefore, cPT and cST exist for each RA.

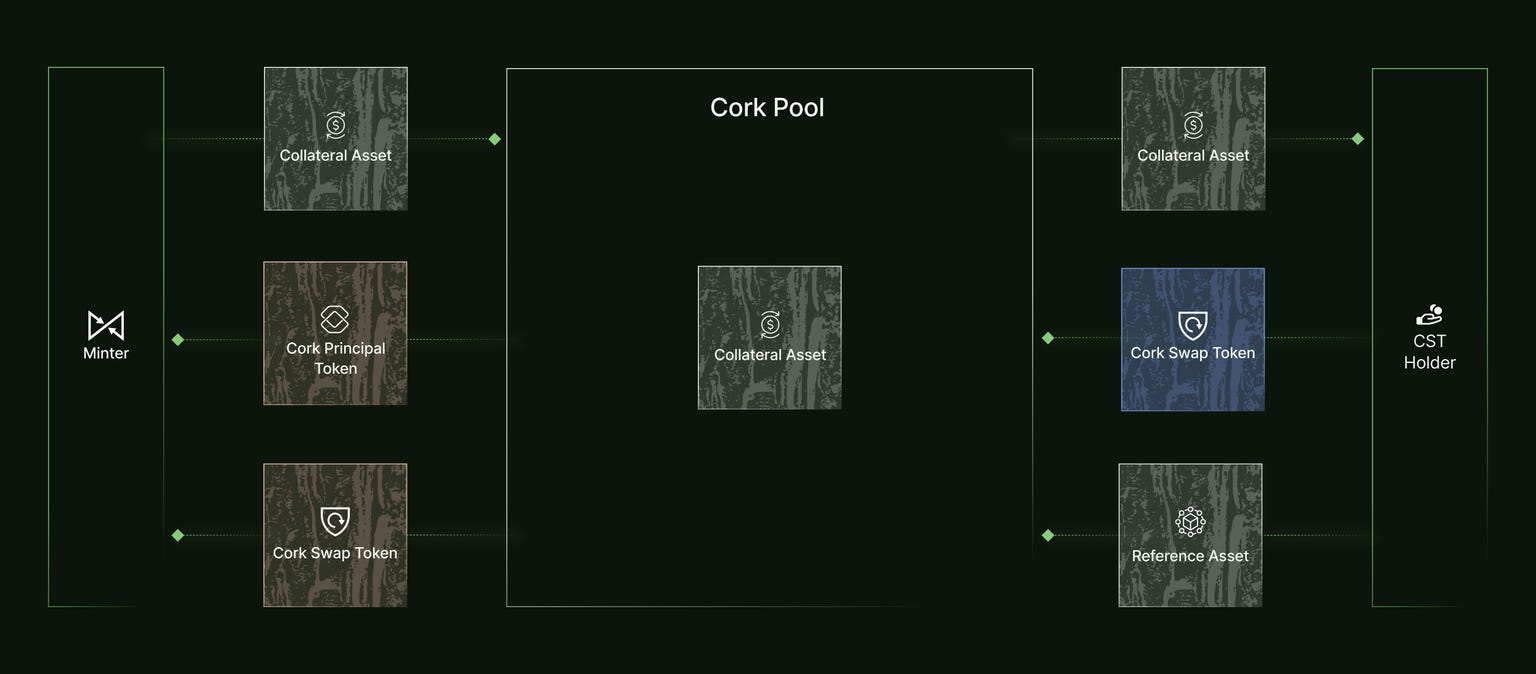

Let me organize things a bit.

Reference Asset (RA): Tokens subject to depegging, such as stSTH.

Collateral Asset (CA): Collateral token for RA depeg insurance.

Cork Principal Token (cPT): Issued upon CA deposit, serving as a token for pool underwriters. Risk bearer during depeg events.

Cork Swap Token (cST): Issued upon CA deposit and serves as a token for pool insurance users.

As for the relationship between each token,

CA = cPT + cST, and when cPT and cST are placed in the pool, CA is returned.

RA + cST = CA, and when you deposit RA and cST during depeg (or at any other time), the corresponding CA is always returned.

Did that make sense? When depegging occurs, the market price of RA plummets. However, with this pool, if you bring RA and cST, they will exchange them for CA at the normal price. That’s precisely why it acts as insurance during depegging.

At that point, cST and the devalued RA are deposited while the CA exits, so naturally the value of the assets within the pool diminishes. cPT holders bear the risk at that time, and their deposited principal is lost.

Conversely, when depegging does not occur, revenue is generated from sources such as “collateral fund investment returns,” “cST sale proceeds,” “swap fees,” “incentive rewards from partners or Cork,” and “re-collateralization investment returns.”

Therefore, the Cork mechanism can also be viewed as a financial option.

cST represents the “right to sell pegged assets at a predetermined rate,” similar to a put option. Conversely, cPT, the counterparty to cST, represents the insurer’s position. It earns a fixed premium income (yield) if no depeg occurs, but its value is impaired when depeg occurs, equivalent to selling a put (short put).

In this way, Cork splits the depeg risk into two tokens, cST and cPT, allowing market participants to adjust their risk exposure by trading these tokens.

Additionally, while a minor point, each Depeg insurance market has a pre-set maturity date (the end date of the coverage period), and cSTs have an expiration date. Upon reaching maturity, the cST becomes invalid, and the corresponding cPT holder gains the right to withdraw the remaining assets from the pool.

Therefore, Cork facilitates risk trading in distinct periods called “epochs.” At the end of each period, a new series of cST and cPT is issued, and liquidity providers roll over (reinvest) their funds as needed.

Additionally, the “exchange rate” between collateral assets (CA) and pegged assets (RA) is defined for each market and can be dynamically adjusted over time or in response to interest rate differentials.

For example, in a market where CA is ETH and RA is Lido’s stETH, stETH increases in value over time due to rewards. Therefore, even if initially “1 stETH + 1 cST = 1 ETH,” the required amount of stETH must decrease (the exchange rate must be lowered) daily to account for the slight appreciation of stETH.

In Cork, you can set up a dedicated Exchange Rate Provider to reflect such price ratios and interest rate differentials in real time.

As a result, the yield difference between collateral assets and pegged assets (in this example, the difference between ETH staking rewards and stETH rewards) is automatically factored into the exchange ratio, preventing the underwriter (cPT holders) from receiving unfair arbitrage profits.

Transition and Outlook

The company operating Cork Protocol is Cork Protocol Inc., a startup founded in 2024. Its headquarters are located in New York City, New York, USA, and the team is based in New York while operating globally.

Four key members have been announced as co-founders. Phil Fogel and Rob Schmitt serve as co-founders and co-CEOs, leading the project’s vision and strategy.

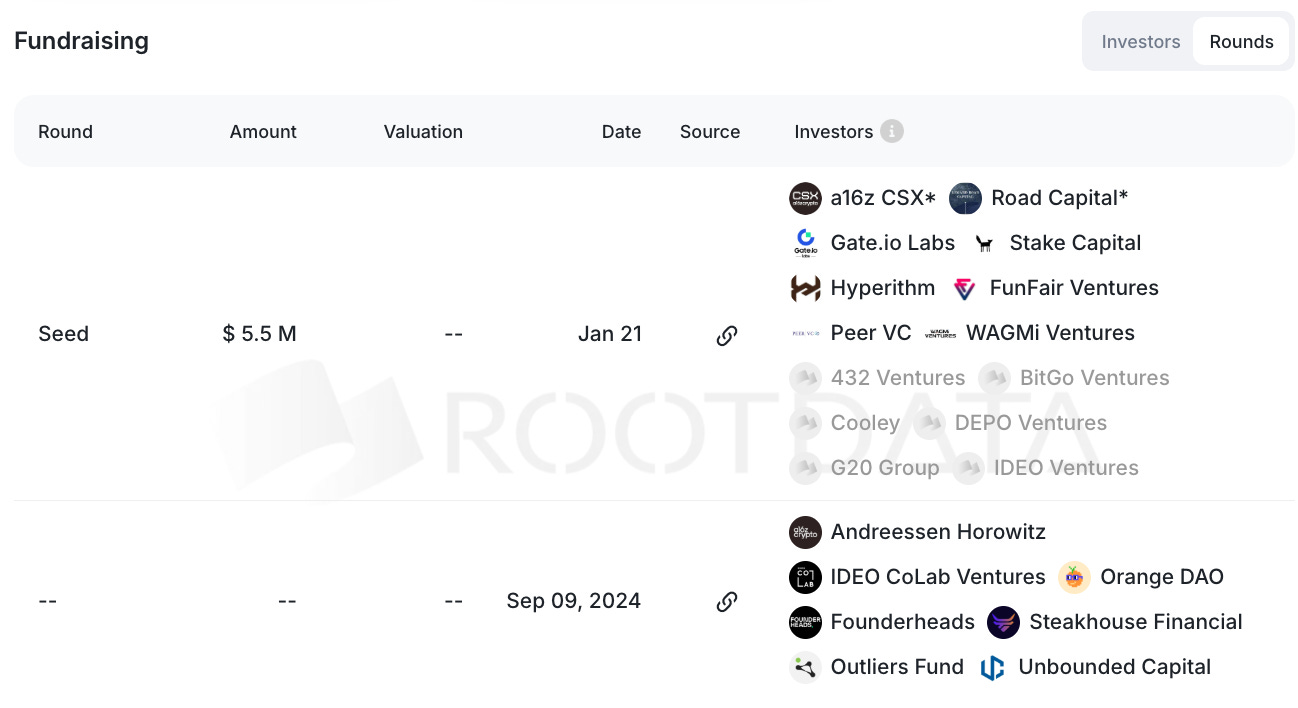

Regarding our funding status, we have raised a total of approximately $7.65 million across two funding rounds to date.

First, in September 2024, the company was selected for the fall cohort of a16z’s crypto accelerator “Crypto Startup School (CSX)” and subsequently raised approximately $2.15 million in seed funding. This round saw participation from multiple web3 investors including a16z Crypto, OrangeDAO, IDEO Ventures, Outliers Fund, Unbounded Capital, and Steakhouse Financial.

Subsequently, in January 2026, the company raised an additional $5.5 million in seed funding. This round was led by Road Capital and the aforementioned a16z CSX Fund. Other global VCs participating in the investment included 432 Ventures, BitGo Ventures, Cooley, Hyperithm, WAGMI Ventures, Stake Capital, and Funfair Ventures.

The protocol is currently operating under a whitelist system, with testing conducted by a limited number of users. However, we are already advancing partnerships and proof-of-concepts with multiple leading projects, and have launched a specific risk market as an actual use case.

For example, in addition to LST-based projects like Lido Finance and Etherfi, we are also collaborating with stablecoin-based projects such as Ethena and Resolv.

However, in May 2025, while operating under the previous protocol, the Cork Protocol suffered a hacking incident that resulted in the unauthorized leakage of approximately $12 million worth of wstETH.

The attacker successfully withdrew approximately 3,762 wstETH using a malicious contract and swapped a portion into ETH. In response, co-founder Phil Vogel immediately announced on X, “We have suspended all contracts while investigating a potential exploit,” preventing further outflow of user funds.

By the end of that year, they launched “Cork Phoenix,” a significantly enhanced security version, restoring the protocol. Following this crisis response, investor and user trust is now gradually being restored.

The specific release schedule for the protocol remains undetermined. However, the company has stated that during its 2026 funding round, it will focus on the full-scale operation of the product and expanding the ecosystem, leading to expectations that the protocol will be released in the near future.

The variety of on-chain insurance products is expanding

Finally, we conclude with a summary and analysis.

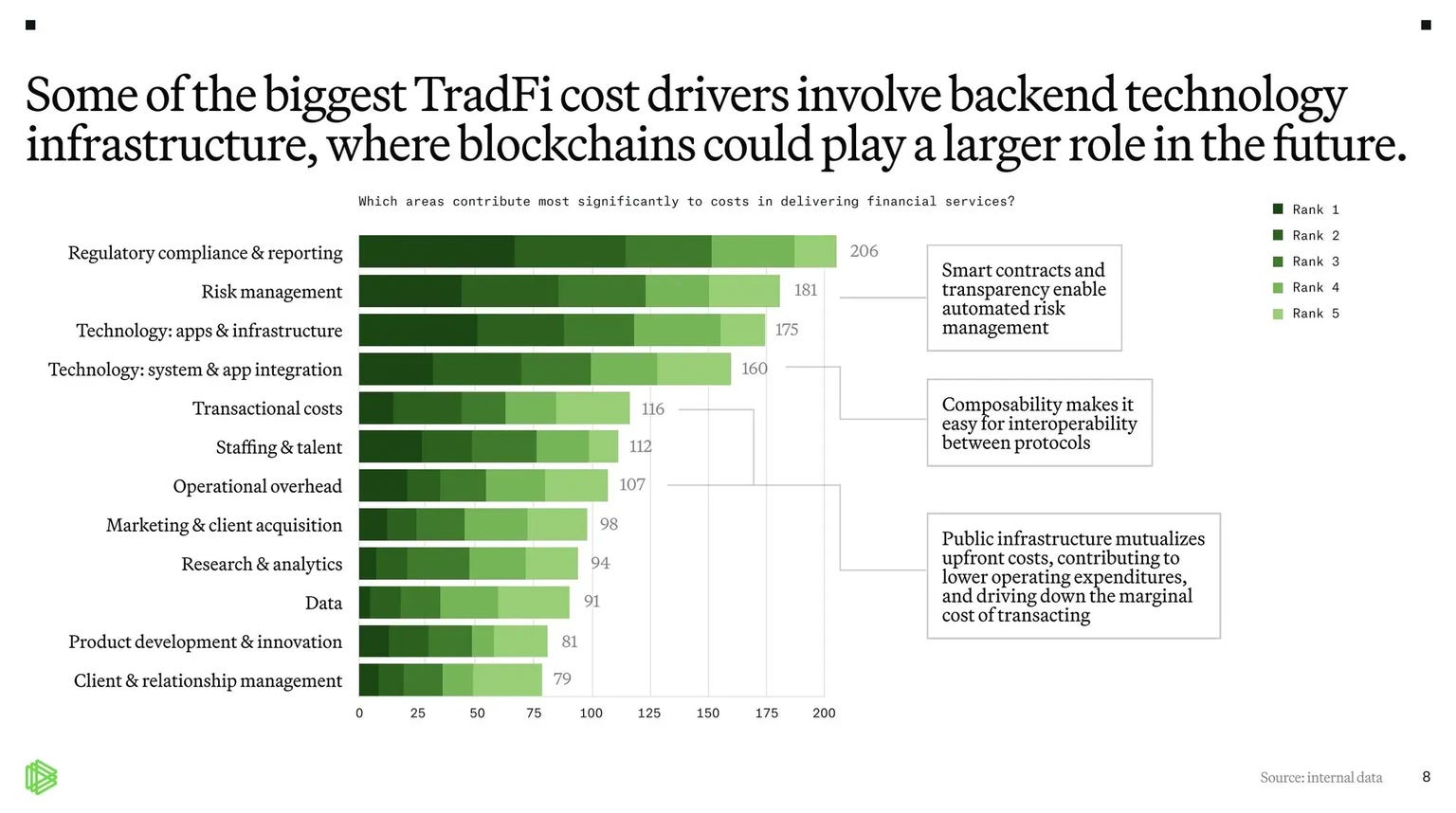

The following diagram is often used to explain the background behind Cork’s founding. It demonstrates with data the argument that “the majority of costs in traditional finance (TradFi) are concentrated in backend systems, where blockchain offers significant structural potential for reduction.”

Specifically, it becomes clear that the costs of financial services are overwhelmingly dominated by back-end operational expenses—such as regulatory compliance, risk management, and system/infrastructure integration—rather than the transactions themselves.

Since 2025, traditional financial institutions and institutional investors have been steadily entering the crypto market. Regulatory compliance is progressing at both the chain level and protocol level, and system/infrastructure integration seems to be largely covered by improvements in the blockchain’s own performance.

However, there are still shortcomings in risk management. Cork sees this very area as holding significant potential.

Indeed, this is true of the futures market, and tracing the origins of all financial instruments often reveals they were born from insurance-like purposes. By financializing future risks, both traders and those seeking to hedge risks create mutually beneficial structures across all industries.

Even in the crypto market, the risk of major tokens depegging is immense. For example, suppose an exchange or ETF manages ETH by converting it to stETH for dual management. While protocol hacking risks naturally exist, there is also the risk of stETH itself depegging. Therefore, a scenario where insurance tokens are purchased to mitigate this risk seems plausible.

Therefore, as more and more things become tokenized and on-chain trading increases, I believe the potential for on-chain insurance products as a risk hedge will also expand. While on-chain insurance has existed for some time, I envision the variety of such products growing.

First, I look forward to the mainnet launch of Cork.

That concludes our research on the Cork Protocol!

Reference Links:HP / DOC / X

Disclaimer:I carefully examine and write the information that I research, but since it is personally operated and there are many parts with English sources, there may be some paraphrasing or incorrect information. Please understand. Also, there may be introductions of Dapps, NFTs, and tokens in the articles, but there is absolutely no solicitation purpose. Please purchase and use them at your own risk.

About us

🇯🇵🇺🇸🇰🇷🇨🇳🇪🇸 The English version of the web3 newsletter, which is available in 5 languages. Based on the concept of ``Learn more about web3 in 5 minutes a day,'' we deliver research articles five times a week, including explanations of popular web3 trends, project explanations, and introductions to the latest news.

Author

mitsui

A web3 researcher. Operating the newsletter "web3 Research" delivered in five languages around the world.

Contact

The author is a web3 researcher based in Japan. If you have a project that is interested in expanding to Japan, please contact the following:

Telegram:@mitsui0x

*Please note that this newsletter translates articles that are originally in Japanese. There may be translation mistakes such as mistranslations or paraphrasing, so please understand in advance.